I just finished the Beta version of the new Portfolio123 extension.

From the help File:

The Portfolio123 extension creates a two-way connection between Wealth-Lab and Portfolio123(https://www.portfolio123.com/index.jsp?apc=DrKoch).

This extension supports the following actions:

* Download historical ranking results that were calculated with a Portfolio123 Ranking System on a specific Universe with a selectable rebalance frequency.

* Create dynamic DataSets from a downloaded ranking, for example the top 50 stocks in each quarter.

* Access fundamental data (contained in the downloaded ranking)

* Create an index indicator in Wealth-Lab and send it as a *Data Series* to Portfolio123

* Calculate an indicator for all symbols in a DataSet and send it as a Stock Factor to Portfolio123

Requirements

* A subscription / membership at Portfolio123.com. (Starts at $25 for first month)

* A historical data provider like Norgate Data(https://norgatedata.com/) that can provide historical prices for the tickers used in your Portfolio123 rankings.

Beta testers write a mail to: rene dot koch at finantic dot de

You'll receive a zip file with the extension.

The extension will run for free until it is finally published.

A beta tester is asked to report:

* experiences

* problems/bugs

* suggestions, comments.

From the help File:

The Portfolio123 extension creates a two-way connection between Wealth-Lab and Portfolio123(https://www.portfolio123.com/index.jsp?apc=DrKoch).

This extension supports the following actions:

* Download historical ranking results that were calculated with a Portfolio123 Ranking System on a specific Universe with a selectable rebalance frequency.

* Create dynamic DataSets from a downloaded ranking, for example the top 50 stocks in each quarter.

* Access fundamental data (contained in the downloaded ranking)

* Create an index indicator in Wealth-Lab and send it as a *Data Series* to Portfolio123

* Calculate an indicator for all symbols in a DataSet and send it as a Stock Factor to Portfolio123

Requirements

* A subscription / membership at Portfolio123.com. (Starts at $25 for first month)

* A historical data provider like Norgate Data(https://norgatedata.com/) that can provide historical prices for the tickers used in your Portfolio123 rankings.

Beta testers write a mail to: rene dot koch at finantic dot de

You'll receive a zip file with the extension.

The extension will run for free until it is finally published.

A beta tester is asked to report:

* experiences

* problems/bugs

* suggestions, comments.

Rename

S&P500 LargeCap (IVV) is missing when selecting Universe.

The combobox for universes shows just a few examples. (The list from here: https://www.portfolio123.com/app/opener/UNIV?cat=-2).

The textbox is writable, you may enter the name of any (existing) Portfolio123 universe.

The textbox is writable, you may enter the name of any (existing) Portfolio123 universe.

Also, you may enter your favourite universes in the file

<WL-Installation-Folder>/Portfolio123/KnownUniverses.xml

The universes-ComboBox gets its contents from that file.

(please send this file back to me after you entered interesting universes)

<WL-Installation-Folder>/Portfolio123/KnownUniverses.xml

The universes-ComboBox gets its contents from that file.

(please send this file back to me after you entered interesting universes)

Can universes be made of their own screens, i.e. contain several filters, including those based on different ranking systems? Or can only standard Universes be used? I don't want to waste quotas for experiments once again))

As far as I understand things:

The connection between Portfolio123 and WealthLab (which is restricted by the available API methods) works as follows:

1.) Create a Universe of stock tickers (or ETF tickers). It is possible to use any combination of Fundamentals and Rules to build such a Universe.

2.) Create a Ranking System. It is possible to use any combination of Fundamentals or other Stock Factors and Data Series to define such a ranking.

3.) The extension downloads ticker and ranking information for the complete (ranked) universe. (Once for each Ranking/universe combination)

4.) The extension constructs dynamic/rebalanced DataSets from the Universe based on the ranking information. (It is possible to build many different DataSets from one ranking/universe)

Example: With a Rebalance Frequency of "One Quarter/Three Months" such a DataSet could contain

the Top 50 Stocks in every quarter for the last 10 years.

It is possible to run a "Buy And Hold" strategy on such a dynamic DataSet.

The result should be very close to a Screener Backtest on Portfolio123.

(But: A Screen/Screener is a different animal and not usable with the Portfolio123 extension.)

The connection between Portfolio123 and WealthLab (which is restricted by the available API methods) works as follows:

1.) Create a Universe of stock tickers (or ETF tickers). It is possible to use any combination of Fundamentals and Rules to build such a Universe.

2.) Create a Ranking System. It is possible to use any combination of Fundamentals or other Stock Factors and Data Series to define such a ranking.

3.) The extension downloads ticker and ranking information for the complete (ranked) universe. (Once for each Ranking/universe combination)

4.) The extension constructs dynamic/rebalanced DataSets from the Universe based on the ranking information. (It is possible to build many different DataSets from one ranking/universe)

Example: With a Rebalance Frequency of "One Quarter/Three Months" such a DataSet could contain

the Top 50 Stocks in every quarter for the last 10 years.

It is possible to run a "Buy And Hold" strategy on such a dynamic DataSet.

The result should be very close to a Screener Backtest on Portfolio123.

(But: A Screen/Screener is a different animal and not usable with the Portfolio123 extension.)

QUOTE:

2.) Create a Ranking System. It is possible to use any combination of Fundamentals or other Stock Factors and Data Series to define such a ranking.

So you're saying I can supply my favorite stocks in step 1) and the Portfolio123 server will figure out a ranking system to find more of the same in step 2)? What do I have to give it in step 2) so it can work this magic?

QUOTE:

So you're saying...

Let me clarify:

Step one is done on Portfolio123.com: Select a starting universe, for example all US Stocks with enough liquidity and a price above $3. You might apply further filters/conditions to create a nice large selection of stocks (or ETFs) called a "Universe".

Step two is also done on Portfolio123.com: You choose some fundamental data and conditions and other "Stock Factors" to build a multi-factor, hierarchical ranking system.

Both steps together result in a "Ranked Univers" and this thing (a large set of tickers, fundamentals and ranks) can be downloaded to Wealth-Lab.

On the Wealth-Lab side of things it is now possible to create a dynamic DataSet based on the "Ranked Universe" which contains something like the Top 100 Stocks rebalanced every quarter (or every month). With all fundamentals that took part in the ranking formula also available as "Event Data" and/or fundamental indicators.

And here starts the interesting story:

Will a trading strategy benefit from such a DataSet?

What fundamentals will improve our strategies?

Q: Is there a free trial period for a Portfolio123 membership that lets me test this new extension?

A: The minimum required membership costs $25 for the first month (Screener membership with 5 years of backtest data).

Q: Is there a special price for Wealth-Lab users?

A: Not yet. But the Portfolio123 people promised to lower the price by 15% if enough people (15 or more) buy some paid membership through this link: https://www.portfolio123.com/index.jsp?apc=DrKoch

This link also enables a 35 days trial (instead of 25 days) but such a trial allows no API access, so the Portfoilo1213 extension can't be used with such a trial.

A: The minimum required membership costs $25 for the first month (Screener membership with 5 years of backtest data).

Q: Is there a special price for Wealth-Lab users?

A: Not yet. But the Portfolio123 people promised to lower the price by 15% if enough people (15 or more) buy some paid membership through this link: https://www.portfolio123.com/index.jsp?apc=DrKoch

This link also enables a 35 days trial (instead of 25 days) but such a trial allows no API access, so the Portfoilo1213 extension can't be used with such a trial.

DrKoch, thank you very much for making this extension.

I have the first results. In P123 I have a subscription "Screener". In P123 I created a universe that gives the following result when tested:

In WL I made a strategy based on this universe

I made the strategy quickly and will continue to refine it.

I have the first results. In P123 I have a subscription "Screener". In P123 I created a universe that gives the following result when tested:

In WL I made a strategy based on this universe

I made the strategy quickly and will continue to refine it.

DrKoch, looks like you’re in contact with P123? Any word on them promoting your excellent extension to their customers?

QUOTE:

I made the strategy quickly

An APR of 37% with a MaxxDD of -16% is just crazy.

Are you sure you didn't heavily over-optimize?

5 years is of course not enough for testing, so it is possible that there is some curve fitting here

DrKoch, I sent you the "Universe" and the ranking system to your email. If you have a subscription for more than 5 years, you can check it out.

DrKoch, can you make it so that it would be possible to make a dataset not only from Universes but also from Screens? Screens can have filters like "Rating("Core: Value")>20", but Universes cannot have such filters. This would greatly improve the capabilities of this extension.

QUOTE:

... but also from Screens?

Sorry, but no. The Portfolio123 API allows the download of historical ranking data only.

There is no download for Screens.

Try to reach your goals with conditions for a Universe plus factors for your Ranking.

Please note: All factors in a ranking are also available on the Wealth-Lab side. So it would be possible to add logic to a Wealth-Lab strategy that uses these factors.

Has anyone gotten such good results like dmitry7?

QUOTE:

Has anyone gotten such good results

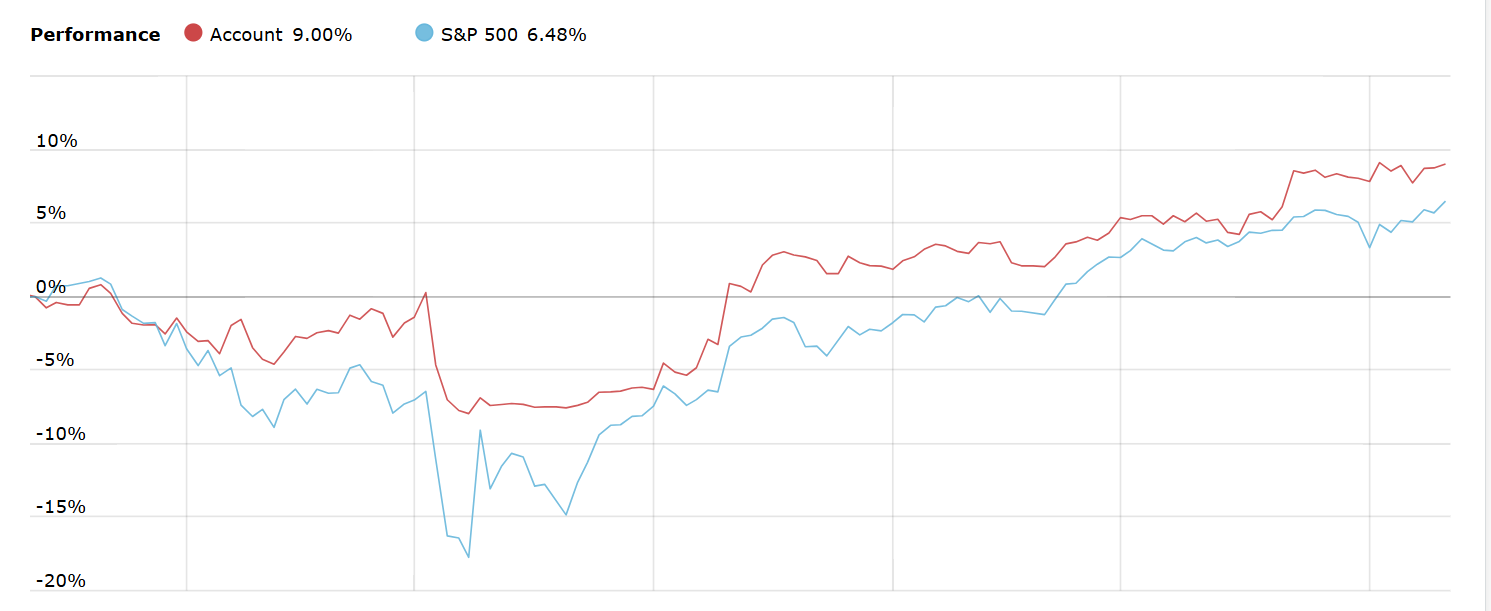

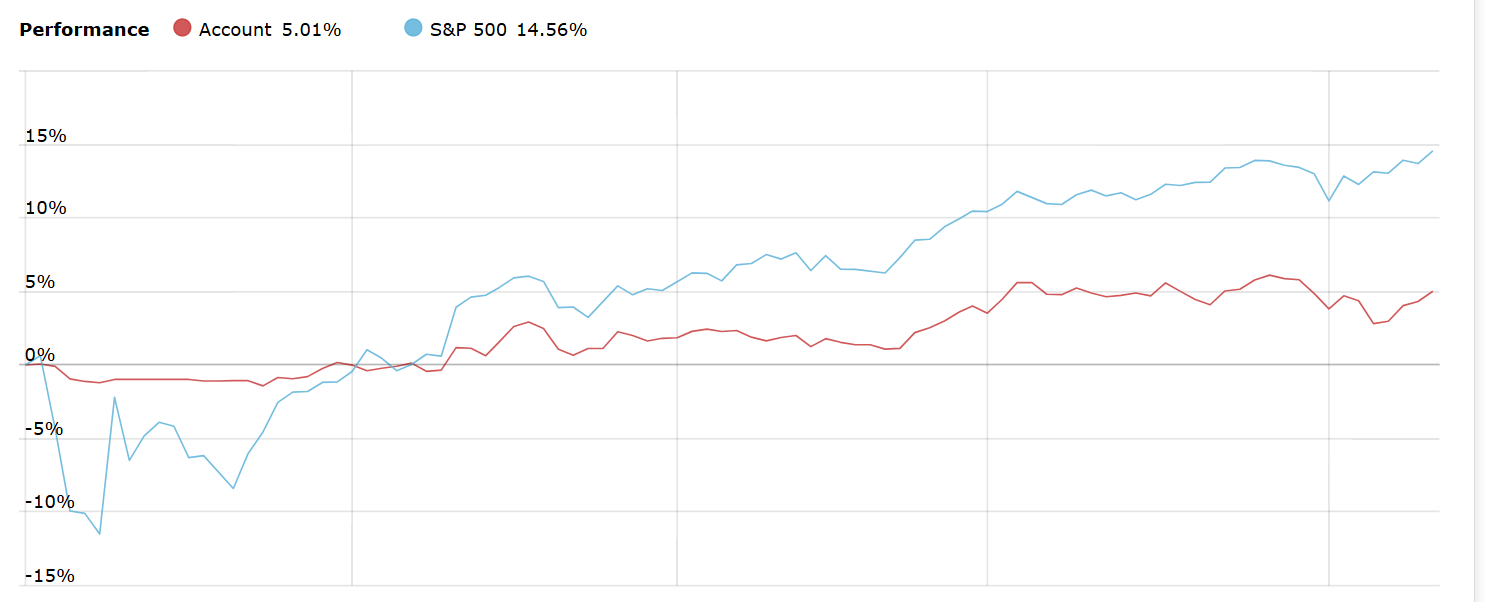

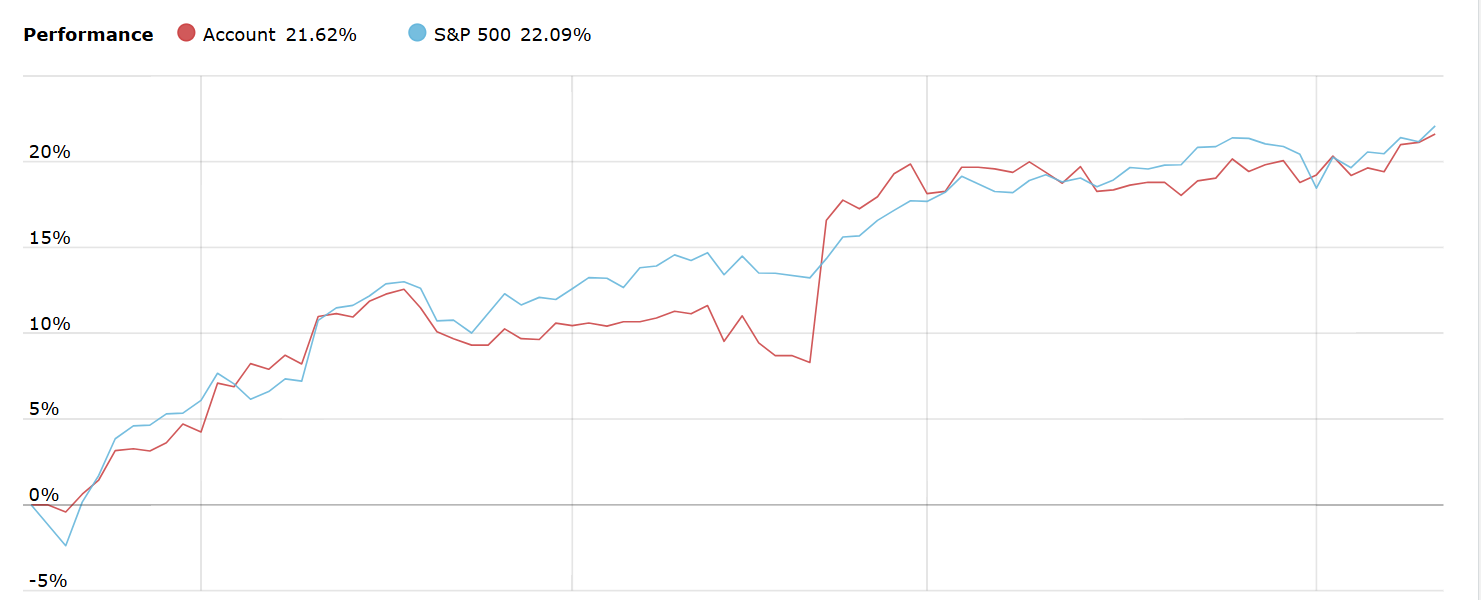

Here is a very quick proof of concept:

I took the "Knife Juggler" strategy from WL's Sample Strategies with its original settings.

(Limit 2%, Timeout 2 bars, PT 5%, no optimization or simliar.)

I ran it for the last 10 years on three different Portfolios/DataSets:

* S&P 100 (WealthData)

* S&P 500 (WeathData)

* a Portfolio123 DataSet called All-Stars: Graham, Top 30 symbols, quarterly rebalanced

Here are the resulting equity curves:

(This is the Compare Tool, part of finantic.ScoreCard extension)

Here the performance metrics of these three runs:

I adjusted position sizes to arrive at roughly the same MaxDrawDown.

I think these results speak for themself.

There was no optimization involved. All settings were "invented" a long time ago.

I adjusted position sizes to arrive at roughly the same MaxDrawDown.

I think these results speak for themself.

There was no optimization involved. All settings were "invented" a long time ago.

Conclusion:

1.) Choice of portfolio/DataSet plays a significant role for performance

2.) Portfolio123 delivers excellent possibilities for selecting a profitable portfolio

3.) The new Portfolio123 extension makes these advantages available for Wealth-lab users

My Personal Summary: The combination of a ranked and rebalanced Portfolio (aka dynamic WL DataSet) and a decent Trading Strategy comes close to the Holy Grail.

1.) Choice of portfolio/DataSet plays a significant role for performance

2.) Portfolio123 delivers excellent possibilities for selecting a profitable portfolio

3.) The new Portfolio123 extension makes these advantages available for Wealth-lab users

My Personal Summary: The combination of a ranked and rebalanced Portfolio (aka dynamic WL DataSet) and a decent Trading Strategy comes close to the Holy Grail.

>comes close to the Holy Grail

It seems so. On one hand, it's too good to be true, on the other, it all makes sense-we combine fundamental and technical analysis to gain the advantages of both. I’ll definitely give it a try. As I understand, since dataset is dynamic it’s better to use the "Exit orphan positions at Market" option here, right?

An idea for Glitch's video series: to test a metastrategy on a such dataset.

@DrKoch, does the extension cache the downloaded datasets to prevent credits from being spent again?

It seems so. On one hand, it's too good to be true, on the other, it all makes sense-we combine fundamental and technical analysis to gain the advantages of both. I’ll definitely give it a try. As I understand, since dataset is dynamic it’s better to use the "Exit orphan positions at Market" option here, right?

An idea for Glitch's video series: to test a metastrategy on a such dataset.

@DrKoch, does the extension cache the downloaded datasets to prevent credits from being spent again?

Good idea, bookmarked!

QUOTE:

does the extension cache the downloaded datasets to prevent credits from being spent again?

Yes. The extension loads a complete historical ranking (ranking system + universe, 10 years back with a backtest membership, selectable rebalance frequency) just once and stores it on the local disk.

From this ranking it is possible to create an unlimited number of dynamic datasets with:

* Number of symbols (example: Top30)

* The ranking metric (any of the fundamentals and stock factors used in the ranking)

* the ranking direction (Best / Worst)

If you have a quarterly rebalanced ranking, and after three months it is time for an update, this will cost just two credits, because the delta (last quarter) is downloaded only.

QUOTE:

Conclusion:

1.) Choice of portfolio/DataSet plays a significant role for performance

This is absolutely true. I always cherry pick my datasets for this reason using the Symbol Rankings tool. For ranking symbols, my favorite ScoreCard metrics are SharpeRatio, WinRate, ATR, and ProfitPerBar.

I have not found an ideal ScoreCard metric that takes everything into account. And I have devised my own ScoreCard metrics in an attempt to do so with marginal success. I'm afraid it's going to take a stat analysis to find the best composite ScoreCard metric to get this ranking business working right. :(

By the way, I'm a trader, not an investor. So what the fundamentals are doing isn't that relevant for my trading. I do check to see that the fundamentals aren't bad (trailing PEG ratio < 2) before pulling the trigger, but that's all. I think Jim Cramer is right; don't try to turn an investment into a trade, and vice versa--they are different.

QUOTE:I disagree, if you take any dip byer system it is very important to separate stocks that are sinking, from good companies that are currently undervalued. Of course, if your trades are shorter than a few days, fundamental data does not play a role here.

By the way, I'm a trader, not an investor. So what the fundamentals are doing isn't that relevant for my trading

QUOTE:

if you take any dip byer system it is very important to separate stocks that are sinking, from good companies that are currently undervalued

This would be a concern if you're trading micro-cap stocks--yes that small company is probably sinking. In contrast, if a mega-cap stock dips (Nvidia, Tesla), it's probably political. :(

Based on such a Universe

I made two strategies. The first strategy is trend-following.

And the second strategy is reversion to the mean.

I made two strategies. The first strategy is trend-following.

And the second strategy is reversion to the mean.

Thanks for posting, dmitry. Looks very promising.

Could you please post the Metrics Report for the second strategy also?

And most important (for me at least):

Could you please describe what data (range) was used for developing, adapting, optimizing?

What is the Out-of-Sample data range?

What was your development method with respect to Insample/Out-of-Sample intervals?

Could you please post the Metrics Report for the second strategy also?

And most important (for me at least):

Could you please describe what data (range) was used for developing, adapting, optimizing?

What is the Out-of-Sample data range?

What was your development method with respect to Insample/Out-of-Sample intervals?

Metrics Report for the second strategy

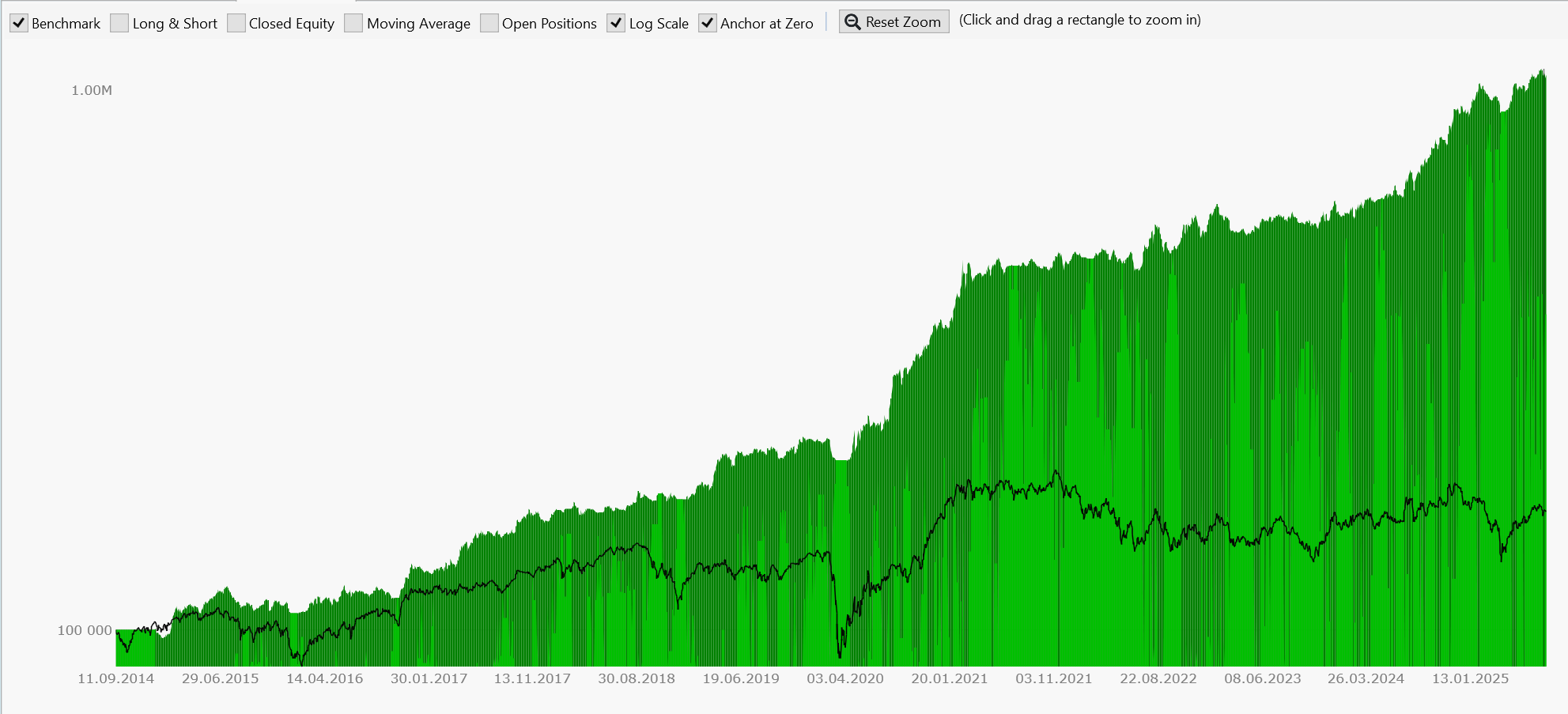

The strategy has been tested for 10 years.

Out of sample missing.

Initially, I created the Universe when I had a subscription Screen, but to download the history for 10 years, I bought a 10-year subscription for one month. And the graph shows that the Universe doesn't look bad even before 2020. I am confident in this strategy because it is based on my strategy in P123, which I have been trading for over a year. Here are the statistics on real transactions using the strategy in P123

I made this strategy in the strategy simulator, but traded using the screen and template with indicators in Tradingview to make decisions about exiting positions. And I calculated stops and take profits in Excel. Now it will be easier to trade using WL.

Here are the characteristics of this strategy in P123 at the time of creation

The new strategy in WL has a slightly different Universe compared to the strategy in P123 and instead of stops and take profits in percentages, ATR is used. Unfortunately, ATR cannot be used in P123.

Dynamic DataSet is updated every 2 weeks.

The strategy has been tested for 10 years.

Out of sample missing.

Initially, I created the Universe when I had a subscription Screen, but to download the history for 10 years, I bought a 10-year subscription for one month. And the graph shows that the Universe doesn't look bad even before 2020. I am confident in this strategy because it is based on my strategy in P123, which I have been trading for over a year. Here are the statistics on real transactions using the strategy in P123

I made this strategy in the strategy simulator, but traded using the screen and template with indicators in Tradingview to make decisions about exiting positions. And I calculated stops and take profits in Excel. Now it will be easier to trade using WL.

Here are the characteristics of this strategy in P123 at the time of creation

The new strategy in WL has a slightly different Universe compared to the strategy in P123 and instead of stops and take profits in percentages, ATR is used. Unfortunately, ATR cannot be used in P123.

Dynamic DataSet is updated every 2 weeks.

QUOTE:

ATR cannot be used in P123

Why not?

In simulated strategies there is no stop based on ATR, only in percentage

During the process of updating historical providers at the moment of updating Portfolio123, an error appears and the WL closes

It's already working. It's possible that at that moment the servers in Portfolio123 were being updated.

DrKoch, can you tell me how to remove the WealthData duplication that appeared after installing the beta version of the extension? Which file needs to be corrected?

Based on the topics that appear here, there seems to be interest in integration, but I've tried using p123 on its own a few times and each time I ended up with some nonsense. It's nowhere near the numbers in dmitry7's posts. Is anyone using this combo in real trading and getting better results than the benchmark and wl alone?

QUOTE:

... I've tried using p123 on its own a few times and each time I ended up with some nonsense.

First the disclaimer: I haven't used Portfolio123 myself.

But as a numerical analysis guy, I can tell you if you try to combine two orthogonal (linearly unrelated) criteria together, you are going to get nonsense in most cases. So don't do that!

You need to carefully pick selection criteria that's related and points in the same direction. Perhaps a Portfolio123 consultant can help you select "correlated" selection criteria that might complement your WL trading strategy better.

From my point of view the story goes like this:

Whenever we construct a "Trading Strategy" we in fact try to predict future price movements.

Such a prediction is based on (some combination) of

* Indicators (the Technical Analysis term, also used by Wealth-Lab)

* Stock Factors (The Portfolio123 term)

* Features (the Machine Learning term, also used by Quants)

(All three terms mean basically the same thing: A time series)

We try to find Indicators/Factors/Features that have some predictive power i.e. are somewhat correlated with future price movements.

Furthermore we try to combine several of these Indicators/Factors/Features and it helps if two factors are as uncorrelated as possible. (i.e contain new information)

Some factors usually used in Wealth-Lab Trading strategies are:

* Changes in price (MOM, ROC, SROC, LInReg, ...)

* Unusual price changes (see limit order systems)

* Changes in volume

* Changes in volatility

* Short Term changes of Price/Volume/Volatility) versus long term changes (see MA crossover systems)

Some factors used not so often are:

* Indicators of a benchmark symbol (i.e. Changes/Volatility of SPY)

* Global Indicators (Interest rates, unemployment rates, the price of gold, ...)

* Volatility ETFs

These categories are rather uncorrelated and make good "inputs" of a trading strategy.

With Portfolio123 we have access to a database with historical fundamental data. (All numbers in Quarterly Business reports).

These numbers change once in three moths.

As far as I can see there are two schools of thought:

1. Value investors: The future of a company can be deducted from its fundamentals. So it makes sense to invest in a company with "good fundamentals"

2. The stock-price-believers: All properties of a company and the beliefs about this company are already reflected by the company's stock price. There is no additional information contained in the quarterly business reports.

If you tend to school #1 you should use the Portfolio123 extension to improve your trading strategy.

If you tend to school #2: Not.

Whenever we construct a "Trading Strategy" we in fact try to predict future price movements.

Such a prediction is based on (some combination) of

* Indicators (the Technical Analysis term, also used by Wealth-Lab)

* Stock Factors (The Portfolio123 term)

* Features (the Machine Learning term, also used by Quants)

(All three terms mean basically the same thing: A time series)

We try to find Indicators/Factors/Features that have some predictive power i.e. are somewhat correlated with future price movements.

Furthermore we try to combine several of these Indicators/Factors/Features and it helps if two factors are as uncorrelated as possible. (i.e contain new information)

Some factors usually used in Wealth-Lab Trading strategies are:

* Changes in price (MOM, ROC, SROC, LInReg, ...)

* Unusual price changes (see limit order systems)

* Changes in volume

* Changes in volatility

* Short Term changes of Price/Volume/Volatility) versus long term changes (see MA crossover systems)

Some factors used not so often are:

* Indicators of a benchmark symbol (i.e. Changes/Volatility of SPY)

* Global Indicators (Interest rates, unemployment rates, the price of gold, ...)

* Volatility ETFs

These categories are rather uncorrelated and make good "inputs" of a trading strategy.

With Portfolio123 we have access to a database with historical fundamental data. (All numbers in Quarterly Business reports).

These numbers change once in three moths.

As far as I can see there are two schools of thought:

1. Value investors: The future of a company can be deducted from its fundamentals. So it makes sense to invest in a company with "good fundamentals"

2. The stock-price-believers: All properties of a company and the beliefs about this company are already reflected by the company's stock price. There is no additional information contained in the quarterly business reports.

If you tend to school #1 you should use the Portfolio123 extension to improve your trading strategy.

If you tend to school #2: Not.

Statistics of real transactions for my several systems in the P123+WL bundle:

These strategies are based on the S&P500 universe

Currently in the process of developing a trend following strategy for mid and small cap stocks:

These strategies are based on the S&P500 universe

Currently in the process of developing a trend following strategy for mid and small cap stocks:

Your Response

Post

Edit Post

Login is required