I open a strategy saved with the building blocks twice. If I now test both (100% the same) strategies, the test results are (slightly) different. There can be no rounding differences because the number of trades is different. How can I document this so that you can fix the error?

A restart does not change the problem. Thanks!

A restart does not change the problem. Thanks!

Rename

Bl

blocks

blocks

settings

The strategy has to be the same. Because I open 2 times the same strategy file.

The strategy has to be the same. Because I open 2 times the same strategy file.

Cannot reproduce. No randomization takes place for me if I rerun this strategy over and over on Dow 30 (current) DataSet using Y! data, with or without NSF engaged in Build 6.

There are zero NSF positions and even choosing "Market open next bar" in Position Sizing isn't required as the default "Close" option works.

P.S. You can attach several screenshots when replying. This would be more convenient than doing multiple posts.

There are zero NSF positions and even choosing "Market open next bar" in Position Sizing isn't required as the default "Close" option works.

P.S. You can attach several screenshots when replying. This would be more convenient than doing multiple posts.

If I reopen, not just rerun the strategy - say by opening two instances of the same strategy and aligning them with Tile Vertical - than the two backtests come a bit different but only if NSF positions are not retained. As expected, with "Retain NSF positions" engaged it doesn't happen. So WL7 works as designed.

I can't say whether WL works as designed. I don't think it's logical if the same test gives 2 different results. because the nsf trades are a hypothesis. without nsf, the real results should be displayed. but - what is real? i have to deal with the nsf in more detail, but i find the specific case here a little bit strange. Nevertheless Thanks Eugene!

The reason that the results are different is because you have too many potential buys and not enough simulated capital. When this happens, WL7 randomized which trades to take because it would have no way of knowing in reality which ones would be filled. So, it cannot possibly know what is "real" in this case.

The NSF positions are there regardless of whether you retain them or not. If you do not retain them, however, then WL7 might go ahead and buy ANOTHER position for a symbol earlier than if you had retained them, depending on the logic of your strategy code.

Hope this makes sense!

The NSF positions are there regardless of whether you retain them or not. If you do not retain them, however, then WL7 might go ahead and buy ANOTHER position for a symbol earlier than if you had retained them, depending on the logic of your strategy code.

Hope this makes sense!

A backtest can change due to NSF Positions with "Retain NSF Positions" checked OR unchecked. In both cases, trades can be rejected due to insufficient buying power. The difference is that they're retained (as described in the Help) in one case and not in the other.

As long as the strategy enters into a condition where a trade is rejected, there's a possibility for a random result IF - this is important - IF you don't assign Transaction.Weight (what we used to call Position.Priority).

(Glitch was faster!)

As long as the strategy enters into a condition where a trade is rejected, there's a possibility for a random result IF - this is important - IF you don't assign Transaction.Weight (what we used to call Position.Priority).

(Glitch was faster!)

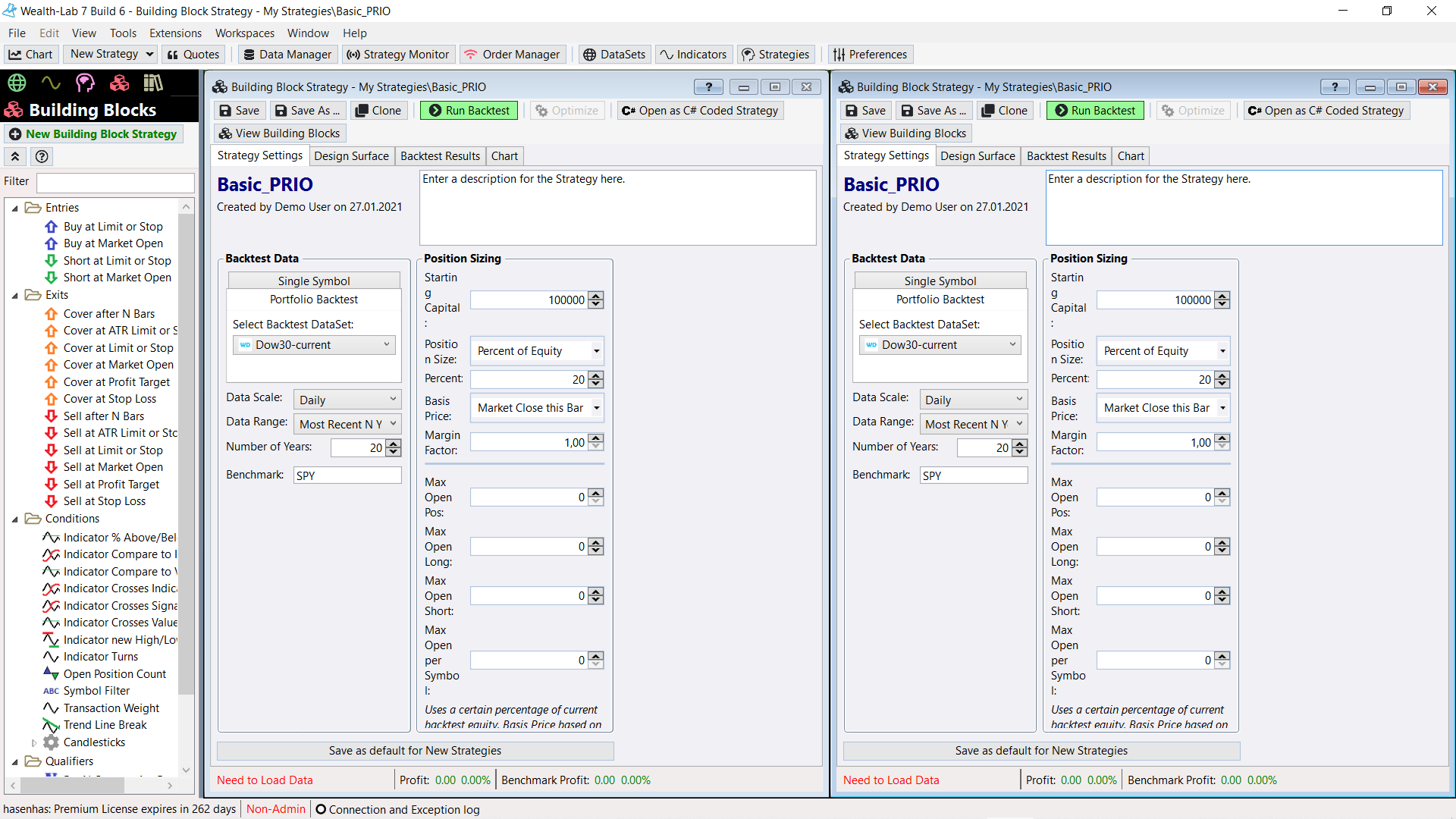

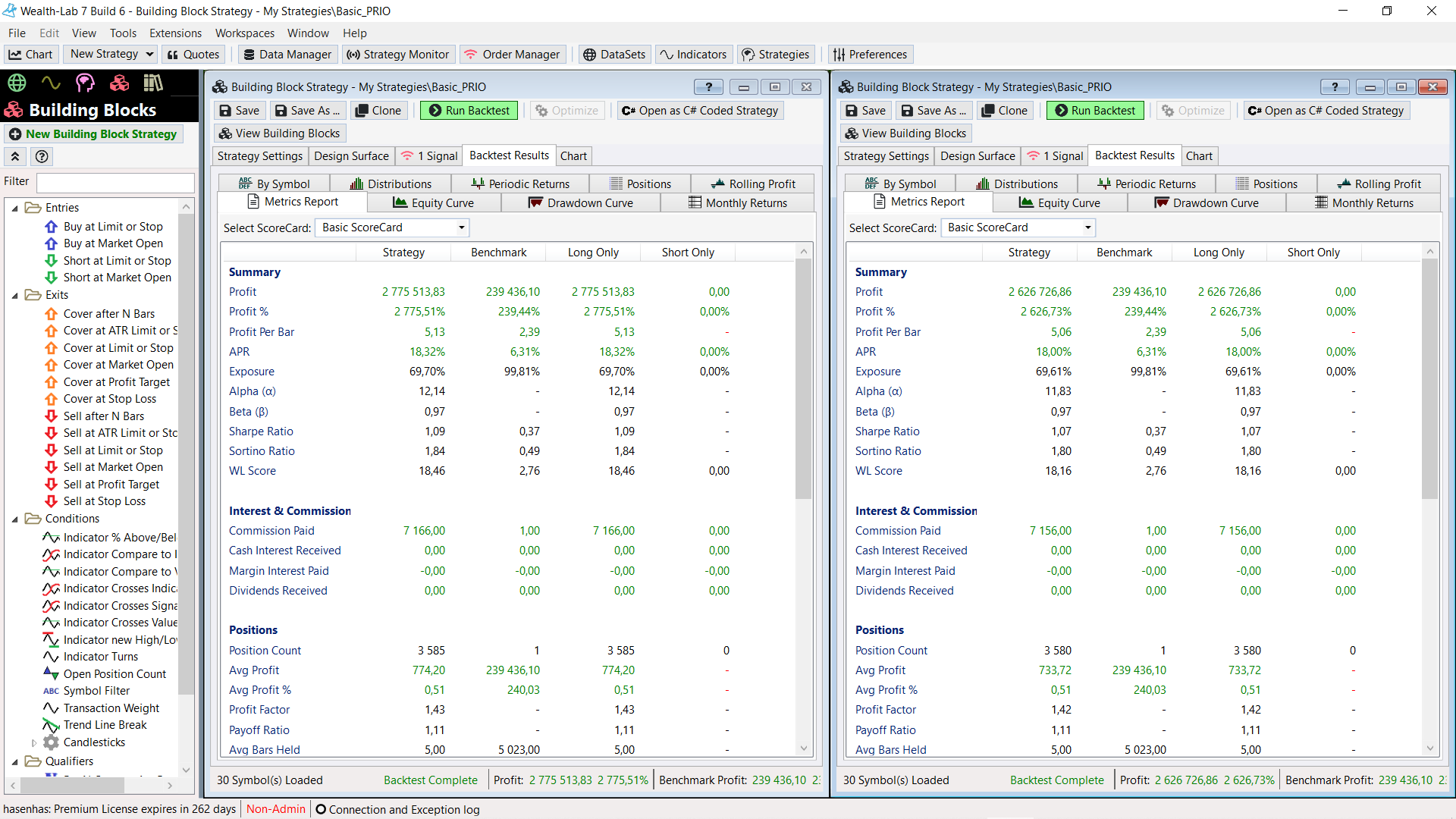

But that shouldn't be the case. Because I use a Transaction Weight (Priority). The results should stay the same. At least that was the case in WL 6.9.

See screenshots above please!

By the way: in Build 7 I haven't had the phenomenon with different results with 100% same strategies (buy on market open & transaction weight) ...

See screenshots above please!

By the way: in Build 7 I haven't had the phenomenon with different results with 100% same strategies (buy on market open & transaction weight) ...

If you found this thread because you had the same question, check out our tutorial video on Transaction Weight - https://youtu.be/ECCF5zdnC7U

Your Response

Post

Edit Post

Login is required