I'm trying to start testing live trading on paper account. I have a monthly rotation strategy, which when I run it in backtest, it generates exits/entry signals for tomorrow (Feb 3, the first trading day of Feb). But when I run it from Strategy monitor by clicking on "Run Now", I do not see any orders being generated, and the strategy deactivate itself after the run. How do I generate orders for tomorrow? Why the strategy deactivate itself?

Rename

To keep a strategy activated after Run Now:

Preferences > Trading > Miscellaneous > Strategy Monitor keeps a Strategy active on Run Now

I set up a Monthly Rotation, and got signals on Run Now. I can't tell what going on with yours.

Preferences > Trading > Miscellaneous > Strategy Monitor keeps a Strategy active on Run Now

I set up a Monthly Rotation, and got signals on Run Now. I can't tell what going on with yours.

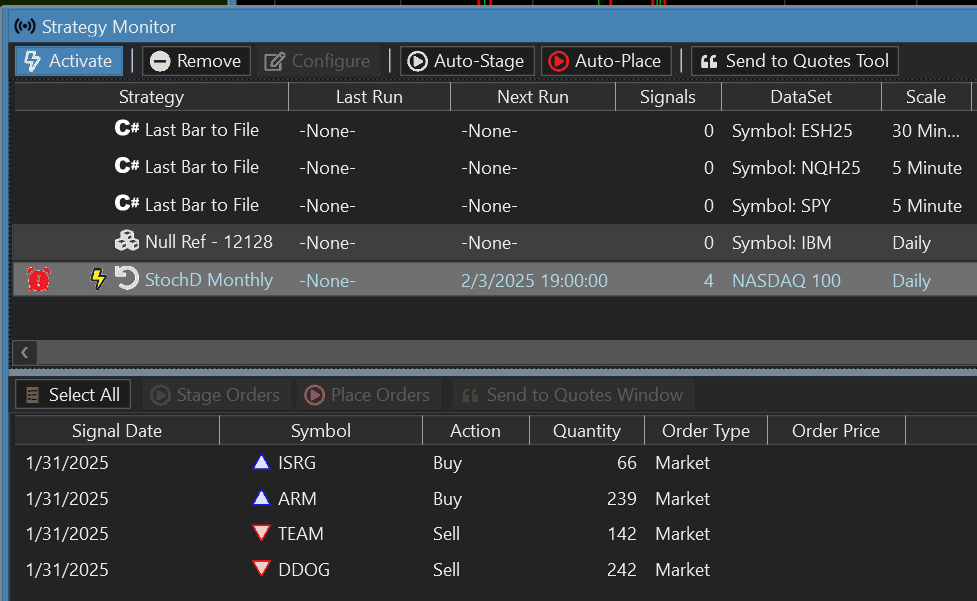

I see the difference. My configuration was with Daily bars using a Monthly rebalance for the Rotation.

You must be running on Monthly bars (fact hidden since you cut off the Scale column in your image). No Signals duplicated - we'll look into it.

You must be running on Monthly bars (fact hidden since you cut off the Scale column in your image). No Signals duplicated - we'll look into it.

Mystery solved. What's your Data Range in the Strategy Monitor Item Configuration?

In my case, I was loading 300 bars, Monthly. It's preliminary, but it seems that the 300 bars are loaded as Daily and then scaled to Monthly, which converts to only 9 or 10 bars. This doesn't happen in the Chart or Strategy Windows, so we'll have to look into it for the S. Monitor.

For now, use a Year or Date Range to load a sufficient amount of data.

In my case, I was loading 300 bars, Monthly. It's preliminary, but it seems that the 300 bars are loaded as Daily and then scaled to Monthly, which converts to only 9 or 10 bars. This doesn't happen in the Chart or Strategy Windows, so we'll have to look into it for the S. Monitor.

For now, use a Year or Date Range to load a sufficient amount of data.

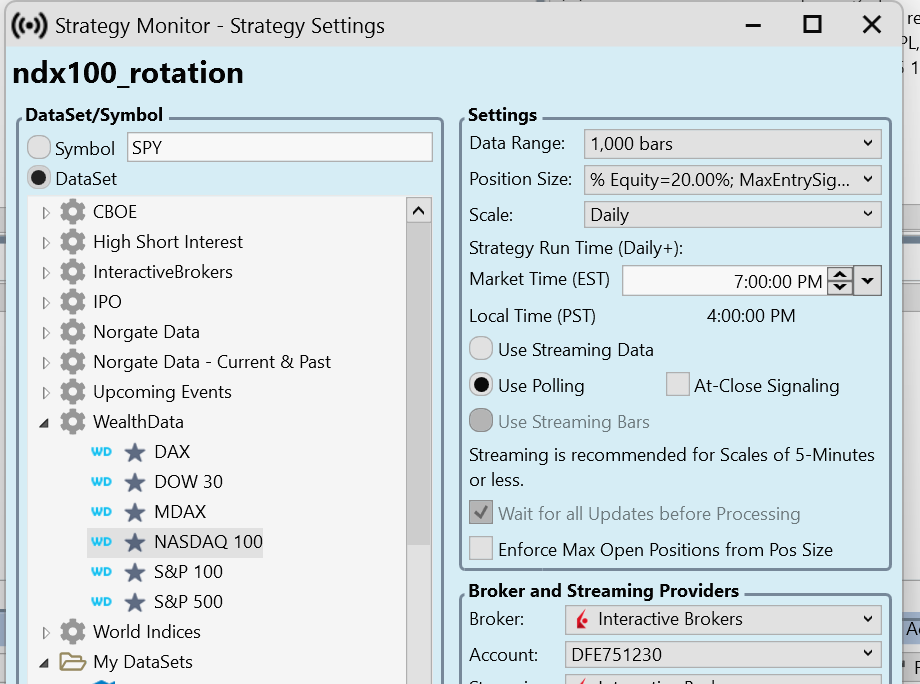

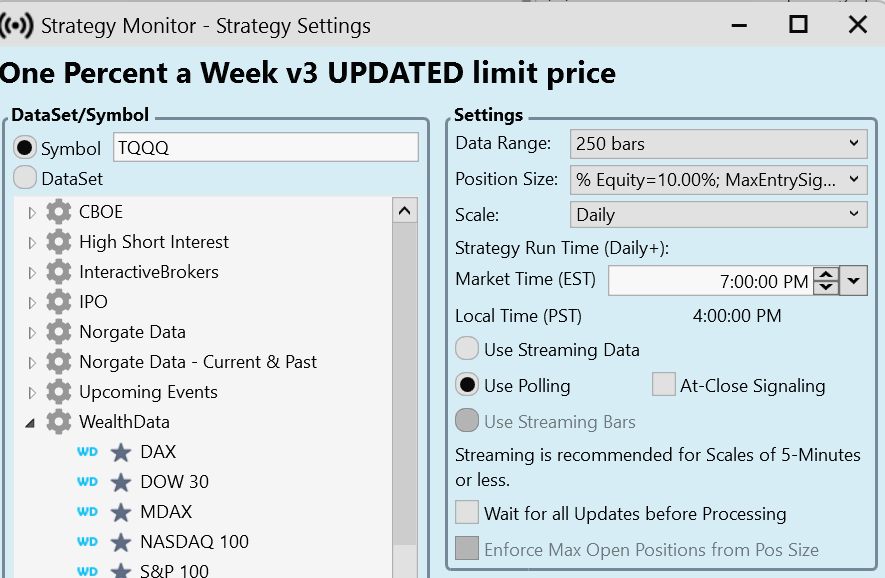

Thanks Cone for looking into this. I actually used Daily in the Scale setting. For the strategy itself, the scale is daily and rebalance frequency is monthly.

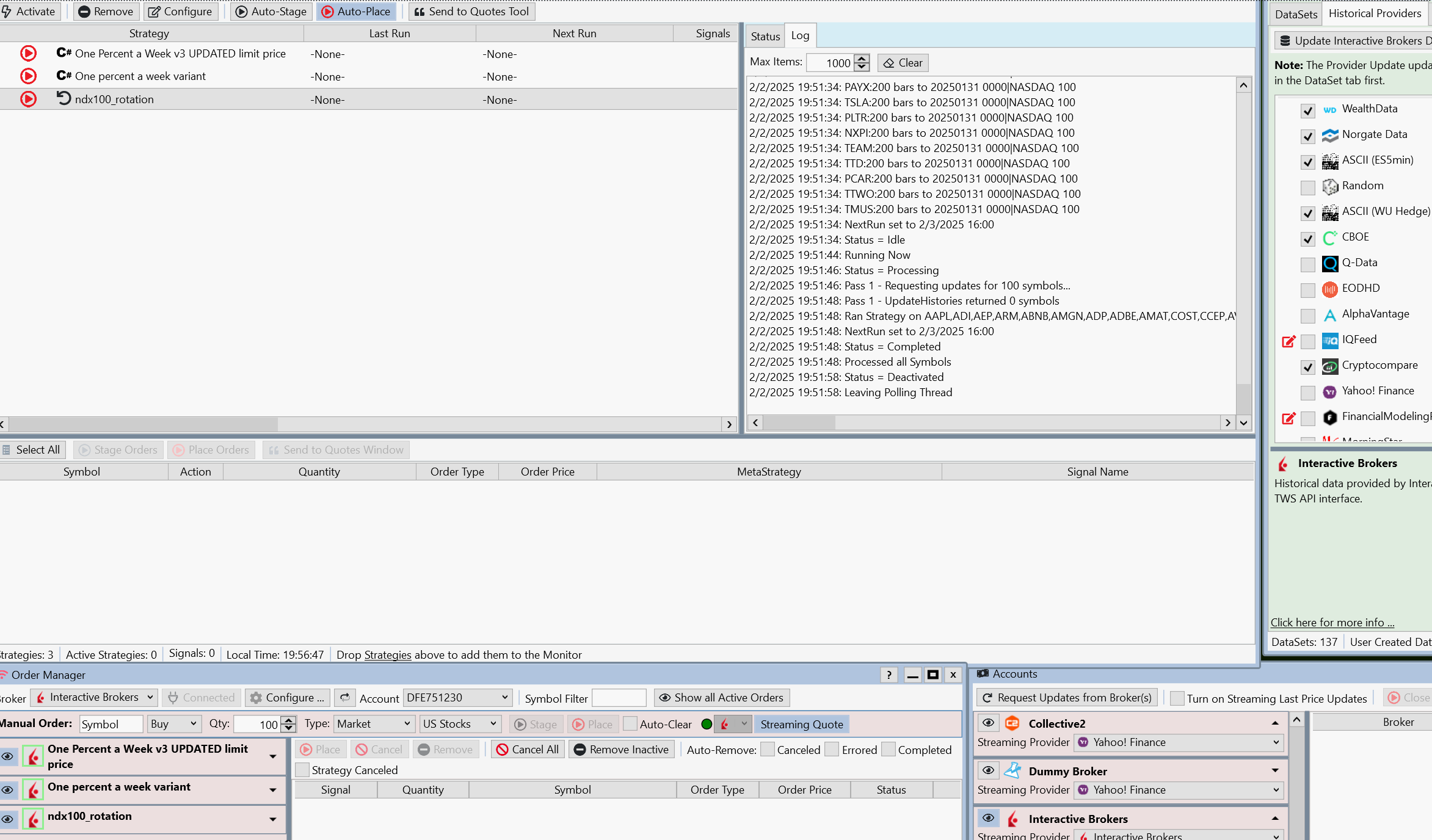

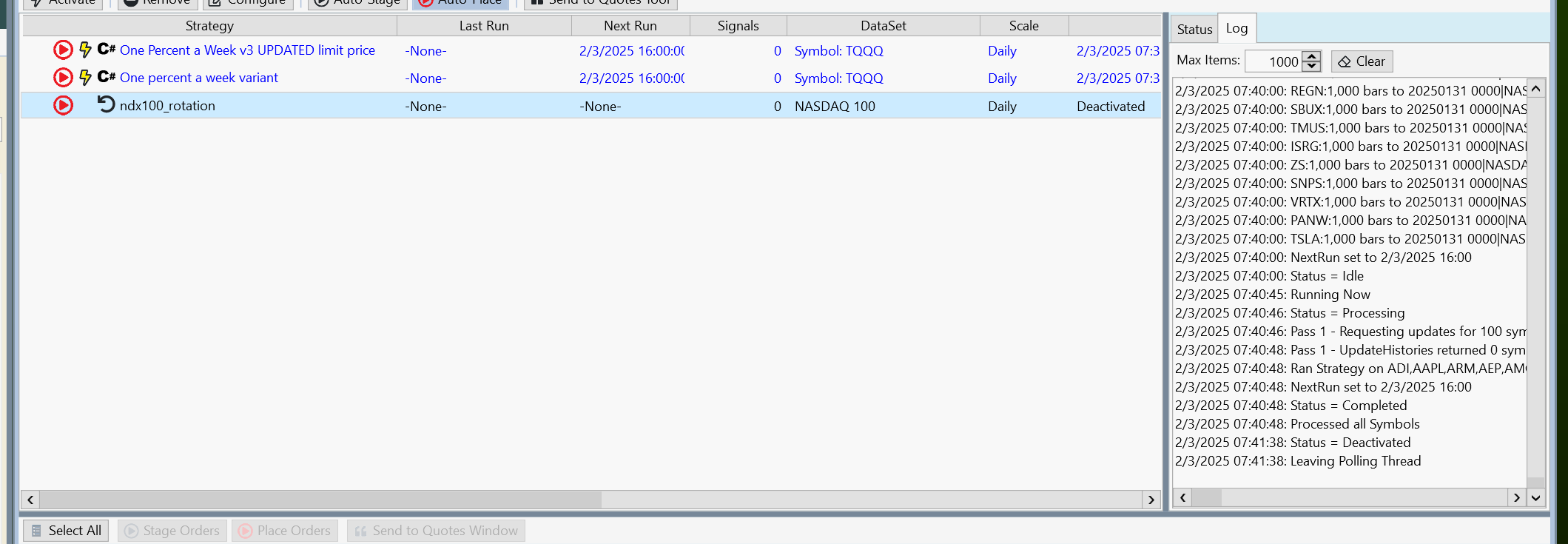

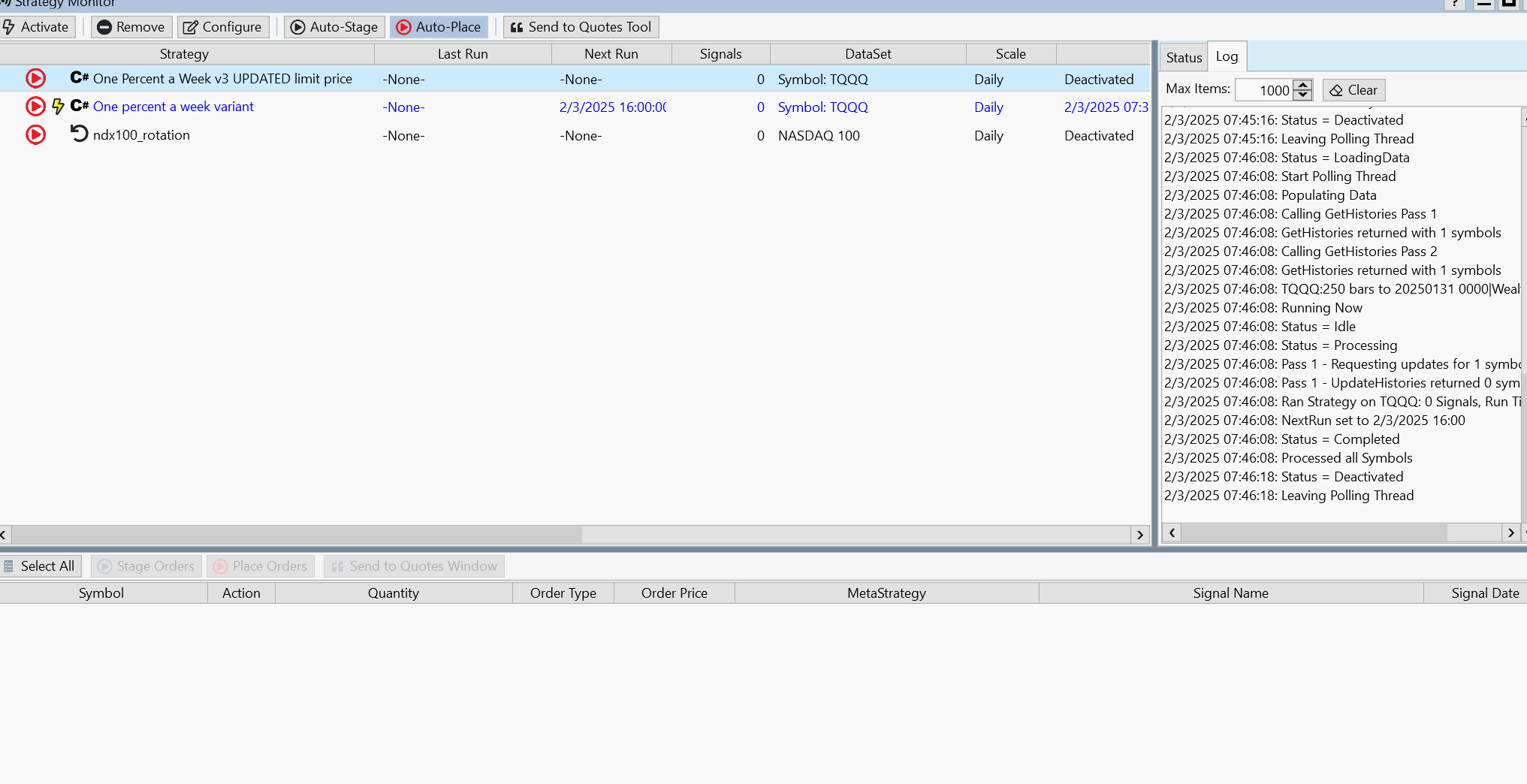

I updated the number of bars to load to 1000 and still got no orders. Checked the config option you mentioned in trading preference, but still the strategy deactivated itself after about 1min.

I updated the number of bars to load to 1000 and still got no orders. Checked the config option you mentioned in trading preference, but still the strategy deactivated itself after about 1min.

Not just the monthly rotation strategy. For the one percent a week strategy I did not get a signal in SM when I just ran it (Run Now) and it deactivated after ran. It generated a signal when I ran the strategy directly.

Is there any related information in the Log Viewer? (I'd guess not, but it's good to check.)

By the way, your modification to One Percent is suspect too. "V3" was programmed with ExecuteSessionOpen(), but you scheduled it outside of market hours. The original V3 strategy will only give you a Signal during market hours after the open. I run it at 09:30:01 - although "Run Now" should work too.

By the way, your modification to One Percent is suspect too. "V3" was programmed with ExecuteSessionOpen(), but you scheduled it outside of market hours. The original V3 strategy will only give you a Signal during market hours after the open. I run it at 09:30:01 - although "Run Now" should work too.

I saw there's one exception in the log viewer, but I think it's unlikely to be from SM since I cleaned the log and rerun and nothing showed up in the log viewer.

Timestamp Source Message Exception

"2/3/2025 07:30:37:860" "Interactive Brokers" "Connected"

"2/3/2025 07:30:41:900" "Interactive Brokers" "07:30:41.90 TWS connected"

"2/3/2025 07:30:42:700" "Interactive Brokers" "07:30:42.70 Market data connections OK: usfarm.nj, usfuture, cashfarm, usfarm, euhmds, fundfarm, ushmds, secdefnj"

"2/3/2025 07:31:00:600" "Norgate Data" "Data Provider: Init (8.0.13)"

"2/3/2025 07:31:00:600" "Norgate Data" "Data Provider: Connected to Norgate Data API"

"2/3/2025 07:31:06:317" "WL8" "Error populating Weights: Unable to cast object of type 'System.Double' to type 'WealthLab.Indicators.IndicatorBase'." "Unable to cast object of type 'System.Double' to type 'WealthLab.Indicators.IndicatorBase'."

"2/3/2025 08:19:15:305" "Yahoo! Finance" "Connected"

Timestamp Source Message Exception

"2/3/2025 07:30:37:860" "Interactive Brokers" "Connected"

"2/3/2025 07:30:41:900" "Interactive Brokers" "07:30:41.90 TWS connected"

"2/3/2025 07:30:42:700" "Interactive Brokers" "07:30:42.70 Market data connections OK: usfarm.nj, usfuture, cashfarm, usfarm, euhmds, fundfarm, ushmds, secdefnj"

"2/3/2025 07:31:00:600" "Norgate Data" "Data Provider: Init (8.0.13)"

"2/3/2025 07:31:00:600" "Norgate Data" "Data Provider: Connected to Norgate Data API"

"2/3/2025 07:31:06:317" "WL8" "Error populating Weights: Unable to cast object of type 'System.Double' to type 'WealthLab.Indicators.IndicatorBase'." "Unable to cast object of type 'System.Double' to type 'WealthLab.Indicators.IndicatorBase'."

"2/3/2025 08:19:15:305" "Yahoo! Finance" "Connected"

Error populating Weights:

- that would de-activate a strategy. When does that one happen?

- that would de-activate a strategy. When does that one happen?

I'll try to reproduce it and report.

I figured out one thing why the 1 percent strategy did not produce a signal. The starting capital in the SM position sizing config was set to $50 somehow. After i changed it to a reasonable value I was able to get a signal (the trading option to use broker account value for position sizing was checked.). After "run now" and getting the signal the strategy deactivate again (something needs to figure out).

This is not he case for the monthly rotation strategy though.

I figured out one thing why the 1 percent strategy did not produce a signal. The starting capital in the SM position sizing config was set to $50 somehow. After i changed it to a reasonable value I was able to get a signal (the trading option to use broker account value for position sizing was checked.). After "run now" and getting the signal the strategy deactivate again (something needs to figure out).

This is not he case for the monthly rotation strategy though.

@Cone

The error is related to the conditional block (Symbol is ranked by). This one was not working before and it was fixed in a recent build after I reported. The exception in the error viewer showed up when I ran the strategy as a standalone but not when I ran it in SM.

When I ran it directly I was able to get backtest results and signals, I did not notice the error until I opened the log viewer.

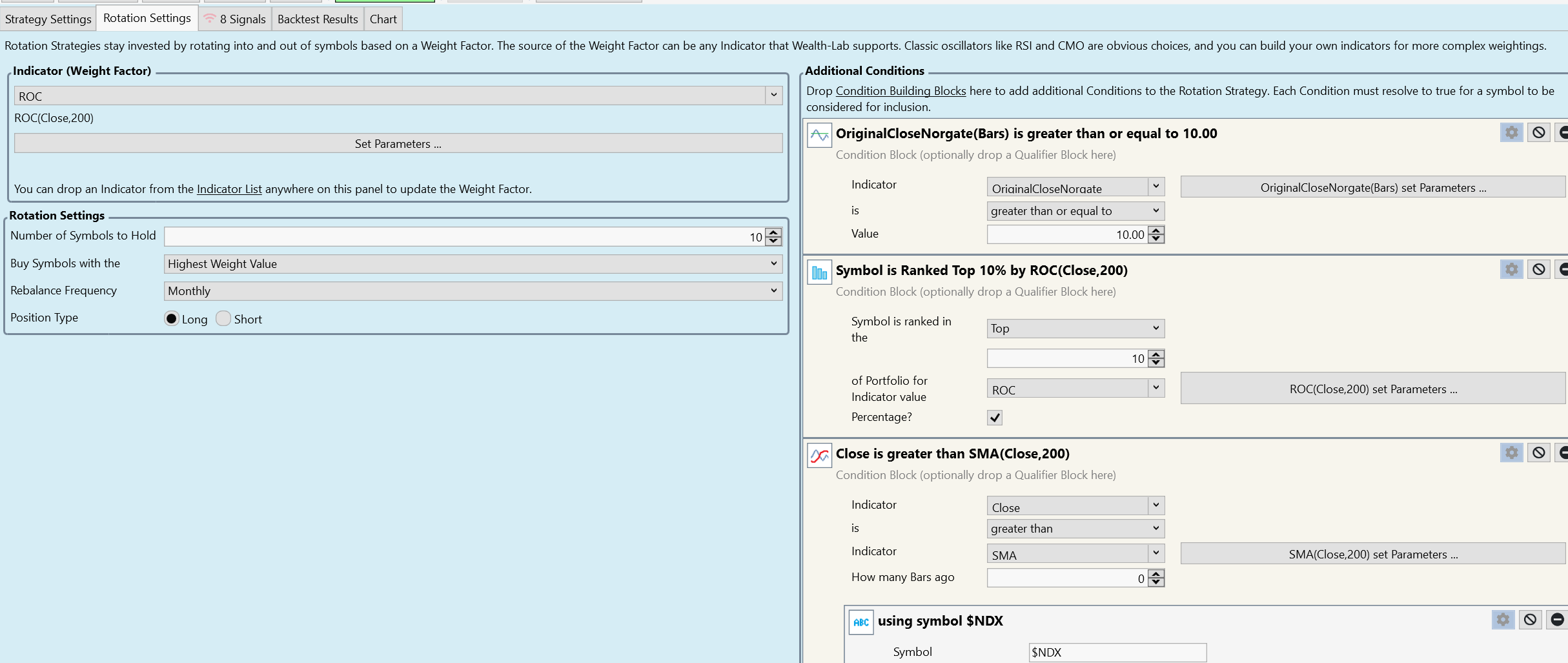

I attached the rules of the rotation strategy that is having issue. It uses Norgate data.

The error is related to the conditional block (Symbol is ranked by). This one was not working before and it was fixed in a recent build after I reported. The exception in the error viewer showed up when I ran the strategy as a standalone but not when I ran it in SM.

When I ran it directly I was able to get backtest results and signals, I did not notice the error until I opened the log viewer.

I attached the rules of the rotation strategy that is having issue. It uses Norgate data.

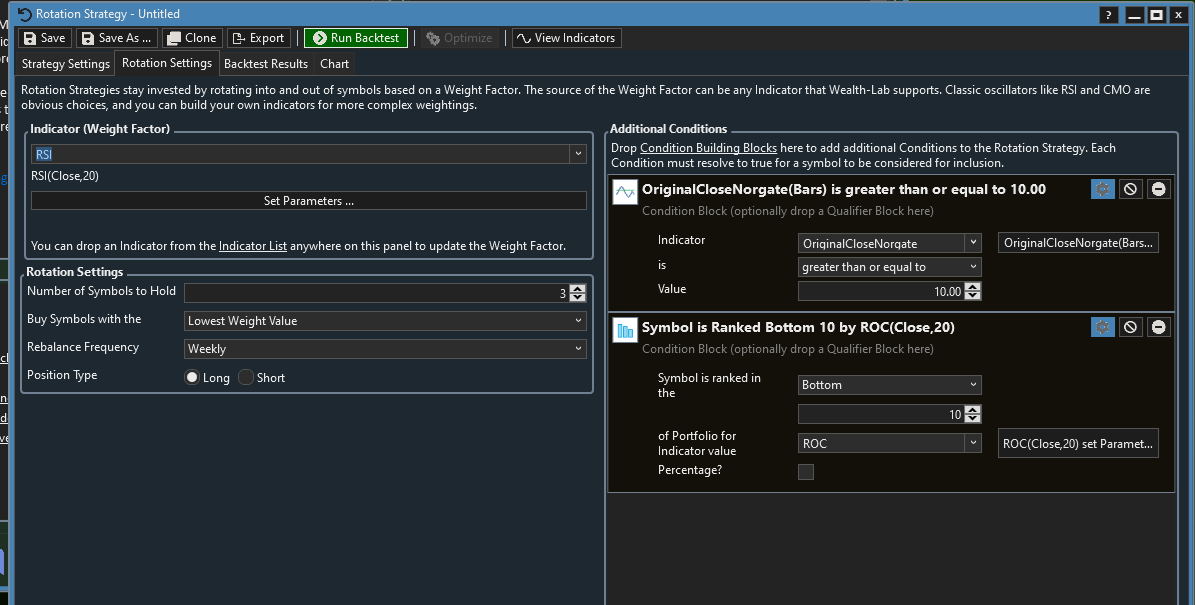

I'm using ROC here both for the weight and the symbol cutoff ranking but actually I'm using different indicators in my own. If using the same indicator one do not have to use the ranking block. Just use this to illustrate the issue.

Some other finding: likely this is also related to Norgate data.

Which Norgate DataSet are you using for the S. Monitor?

Is it a "Past and Present"?

Is it a "Past and Present"?

yes Nasdaq 100 Past & Current

It "should" work but something about Norgate data is throwing an error.

Use the Nasdaq 100 current list. The Strategy Monitor is only giving you current signals anyway. What's in the past is in the past.

Use the Nasdaq 100 current list. The Strategy Monitor is only giving you current signals anyway. What's in the past is in the past.

i changed to current, still get the "Error populating Weights: Unable to cast object of type 'System.Double' to type 'WealthLab.Indicators.IndicatorBase" error. This is related to the symbol ranking conditional block in the rotation strategy. I think there's bug here.

The Symbol Ranking Block is working fine for me in a Rotation. Can you email your exported strategy to support@wealth-lab.com so I can try it?

The problem is that it doesn't happen for me either.

@glitch @cone did you check log viewer? any errors there? As I said the backtest runs fine but I see the above error in log viewer when there's a ranking block. I'm not sure wethere that's related to the auto deactivation in SM.

For me there's no error and it does not de-activate.

Your Response

Post

Edit Post

Login is required