The finantic.Eval extension now supports complete Expressions with operations like addition, multiplication and internal functions like Max(), Min() Abs() and so forth.

The Eval() indicator can replace the IndOnInd(), MathIndOpInd() and MathIndOpValue() transformer indicators and allows for complex indicator combinations:

As an example, here an interesting Time Series for use as the limit price of limit entry orders:

"Open - Max(Open * 0.02, ATR(12) * 0.6)"

Before Build 2 of finantic.Eval you could not do this with Building Blocks and even with a coded strategy it could produce some headache...

See https://www.wealth-lab.com/extension/detail/finantic.Eval for details.

The Eval() indicator can replace the IndOnInd(), MathIndOpInd() and MathIndOpValue() transformer indicators and allows for complex indicator combinations:

As an example, here an interesting Time Series for use as the limit price of limit entry orders:

"Open - Max(Open * 0.02, ATR(12) * 0.6)"

Before Build 2 of finantic.Eval you could not do this with Building Blocks and even with a coded strategy it could produce some headache...

See https://www.wealth-lab.com/extension/detail/finantic.Eval for details.

Rename

Very good work!

Makes WL8 much more flexible, love to see it!

Been experimenting with this and really appreciate this extension. Is there any possibility of supporting strategy optimization? I'd like to be able to optimize the number of bars passed to the indicators inside Eval(...)

I like the decorator pattern. I still do, but this is great work!

QUOTE:

Is there any possibility of supporting strategy optimization?

Yes, of course.

Eval() accepts a string with an indicator expression like "RSI(20)".

In your coded strategy you could have a parameter for the RSI period:

CODE:

double rsiPeriod = Parameters[0].AsDouble;

Now pass this parameter value to the RSI call in Eval():

QUOTE:

Eval($"RSI({rsiPeriod})")

(Note the $ before the string, which triggers String Interpolation)

This works for coded strategies. If you have a Building Block strategy I'd suggest to convert it to a C# Strategy (click "Open as C# Coded Strategy) and (if not alraedy there) add the parameters you need, just for the optimization:

in the constructor or in Initialize():

QUOTE:

AddParameter("rsiPeriod", ParameterType.Double, 5, 1, 25, 1);

I dreamed a bit about optimizable parameters for the Eval() indicator in Building Blocks but finally decided against it because it was too complicated and too ugly and not elegant enough and so forth ... :(

Hi @Profit1000,

you said:

What does the decorator pattern have to do with the Eval() indicator?

you said:

QUOTE:

I like the decorator pattern

What does the decorator pattern have to do with the Eval() indicator?

QUOTE:

What does the decorator pattern have to do with the Eval() indicator?

A way to write clean and structured code before Eval()

DrKoch, thank you for adding EvalOpt in the latest release! I've been using it a lot already, it's greatly appreciated.

QUOTE:

Is there any possibility of supporting strategy optimization? I'd like to be able to optimize the number of bars passed to the indicators inside Eval(...)

Yes, this is available with Build 3 of finantic.Eval

I am trying to get the Min(Open, Close) using Eval, but nothing seems to be working.

It says "expected: Bars" for parameter 1, but if I do Min(Bars, Open, Close) it doesn't seem to give me the Minimum of the current Open and Close. I've tried Math.Min(Open, Close), but it looks like Eval doesn't accept Math functions.

Thank you for your help.

It says "expected: Bars" for parameter 1, but if I do Min(Bars, Open, Close) it doesn't seem to give me the Minimum of the current Open and Close. I've tried Math.Min(Open, Close), but it looks like Eval doesn't accept Math functions.

Thank you for your help.

Try this:

... don't ask ...

CODE:

Min(Bars, Open, Close)

... don't ask ...

Thanks for the clarification. I think I may be running into some sort of bug.

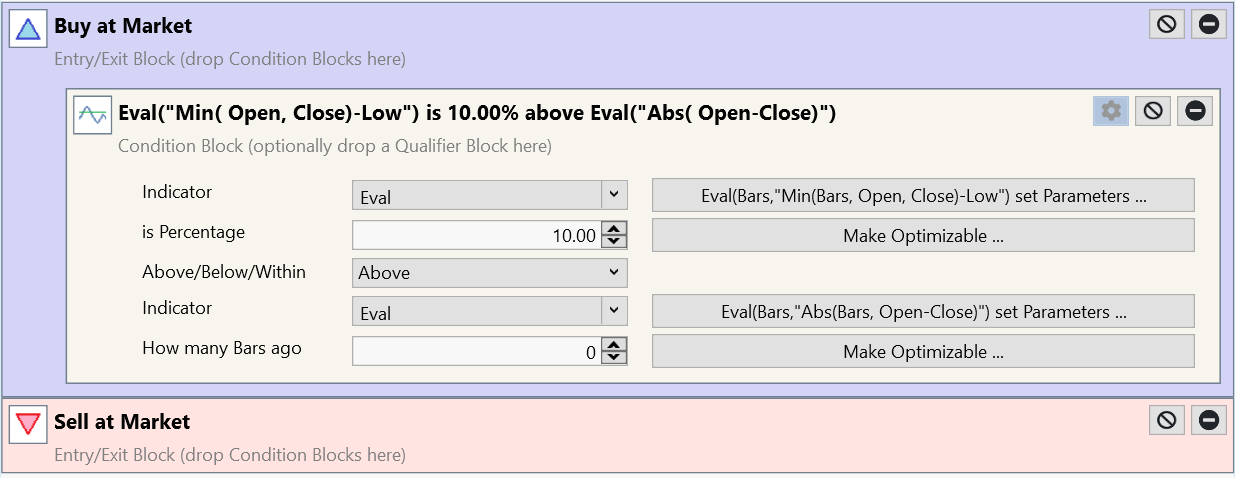

I am trying to check for situations where the lower wick is larger than the candle body. This is how I've set it up:

However, this strategy never enters into any position, even when it should. When I try converting it to a coded strategy and running that, it returns this error:

I think perhaps some aspect of the Eval code is handling the index incorrectly. Here's the generated Execute() function in case it's helpful to see:

I am trying to check for situations where the lower wick is larger than the candle body. This is how I've set it up:

However, this strategy never enters into any position, even when it should. When I try converting it to a coded strategy and running that, it returns this error:

CODE:

Execute Exception (BIP-20DEC30-CDE,0) Line 47 - Index was out of range. Must be non-negative and less than the size of the collection. (Parameter 'index') at WealthLab.Core.DateSynchedList`1.get_Item(Int32 idx) at WealthScript3.MyStrategy.Execute(BarHistory bars, Int32 idx) in :line 47 at WealthLab.Backtest.UserStrategyExecutor.CallWatcher(List`1 lst, DateTime dt)

I think perhaps some aspect of the Eval code is handling the index incorrectly. Here's the generated Execute() function in case it's helpful to see:

CODE:

public override void Execute(BarHistory bars, int idx) { int index = idx; Position foundPosition0 = FindOpenPosition(0); bool condition0; if (foundPosition0 == null) { condition0 = false; { if (index - 0 >= 0) { outcome = false; if (indicator2[index - 1] >= 0) { if (indicator1[index] > indicator2[index - 0] * (1.0 + (10.00 / 100.0))) outcome = true; } else { if (indicator1[index] < indicator2[index - 0] * (1.0 + (10.00 / 100.0))) outcome = true; } } if (outcome) { condition0 = true; } } if (condition0) { Backtester.CancelationCode = 1; _transaction = PlaceTrade(bars, TransactionType.Buy, OrderType.Market, 0, 0, "Buy At Market (1)"); } } else { { Backtester.CancelationCode = 1; ClosePosition(foundPosition0, OrderType.Market, 0, "Sell At Market (1)"); } } }

I was able to reproduce this error outside of using Eval, so I will make a separate thread to inquire further. Thanks again for making the Eval extension, DrKoch.

Your Response

Post

Edit Post

Login is required