In a recent post (see https://www.wealth-lab.com/Discussion/Do-Stocks-Outperform-Treasury-Bills-13029) I showed a plot "#Symbols vs. CAGR".

If you want to see that plot for

* another DataSet

* another benchmark

* another Data Range

You can generate such a plot yourself with WealthLab and the finantic.InteractiveGraphics extension.

In this thread I am going to explain in detail how such a plot is generated.

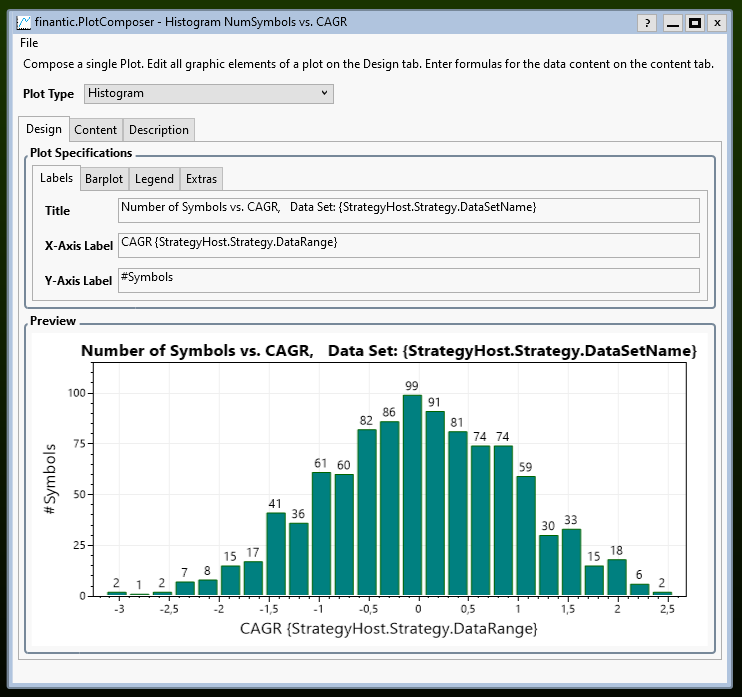

Step 1: Open Extensions->PlotComposer. Select "Histogram" as the Plot Type.

In the "Design" tab, select "Labels" and specify meaningfull texts for "Title", "X-Axis Label and "Y-Axis Label".

At this stage the window should look like this:

Please note how the title reflects the current DataSet. This is done by including the magic pattern

If you want to see that plot for

* another DataSet

* another benchmark

* another Data Range

You can generate such a plot yourself with WealthLab and the finantic.InteractiveGraphics extension.

In this thread I am going to explain in detail how such a plot is generated.

Step 1: Open Extensions->PlotComposer. Select "Histogram" as the Plot Type.

In the "Design" tab, select "Labels" and specify meaningfull texts for "Title", "X-Axis Label and "Y-Axis Label".

At this stage the window should look like this:

Please note how the title reflects the current DataSet. This is done by including the magic pattern

CODE:

{StrategyHost.Strategy.DataSetName}

Rename

Step2: Content of Plot

In the "Content" tab we open "C# Code. (While Interactive Graphics can genrate simpler graphics without coding, the plot at hand is more complex and needs some C# coding.

We are going to use a StringBuilder, so we need "System.Text" in "Usings List:

We collect our histogram data in a List that is decared in the "Variables List":

In the "Content" tab we open "C# Code. (While Interactive Graphics can genrate simpler graphics without coding, the plot at hand is more complex and needs some C# coding.

We are going to use a StringBuilder, so we need "System.Text" in "Usings List:

We collect our histogram data in a List that is decared in the "Variables List":

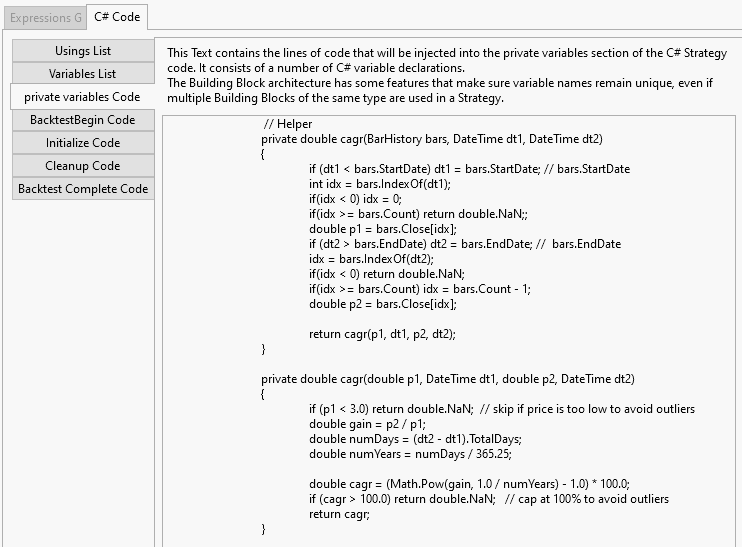

Calculation of CAGR

All these BarHistories have varying start and end dates, so we can't use an Indicator for the CAGR calculation. Instead we use a helper routine that accepts dates and prices:

(see https://en.wikipedia.org/wiki/Compound_annual_growth_rate for the calculation details)

We are going to calculate CAGR for BarHistories and use another helper to make things simpler:

Both routines go to the "private variables Code" section:

All these BarHistories have varying start and end dates, so we can't use an Indicator for the CAGR calculation. Instead we use a helper routine that accepts dates and prices:

CODE:

private double cagr(double p1, DateTime dt1, double p2, DateTime dt2) { if (p1 < 3.0) return double.NaN; // skip if price is too low to avoid outliers double gain = p2 / p1; double numDays = (dt2 - dt1).TotalDays; double numYears = numDays / 365.25; double cagr = (Math.Pow(gain, 1.0 / numYears) - 1.0) * 100.0; if (cagr > 100.0) return double.NaN; // cap at 100% to avoid outliers return cagr; }

(see https://en.wikipedia.org/wiki/Compound_annual_growth_rate for the calculation details)

We are going to calculate CAGR for BarHistories and use another helper to make things simpler:

CODE:

private double cagr(BarHistory bars, DateTime dt1, DateTime dt2) { if (dt1 < bars.StartDate) dt1 = bars.StartDate; // bars.StartDate int idx = bars.IndexOf(dt1); if(idx < 0) idx = 0; if(idx >= bars.Count) return double.NaN;; double p1 = bars.Close[idx]; if (dt2 > bars.EndDate) dt2 = bars.EndDate; // bars.EndDate idx = bars.IndexOf(dt2); if(idx < 0) return double.NaN; if(idx >= bars.Count) idx = bars.Count - 1; double p2 = bars.Close[idx]; return cagr(p1, dt1, p2, dt2); }

Both routines go to the "private variables Code" section:

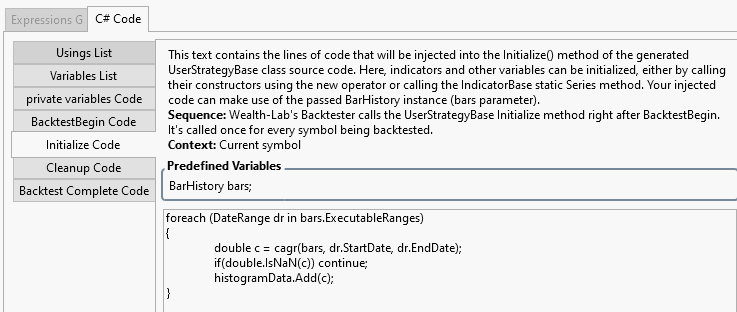

With the calculation routines in place we can actually calculate and collect the CAGR values for each symbol. The code for that goes to the "Initialize Code" section:

Here is the code:

Please note: The individual CAGR values are collected in the histogramdata list.

Here is the code:

CODE:

foreach (DateRange dr in bars.ExecutableRanges) { double c = cagr(bars, dr.StartDate, dr.EndDate); if(double.IsNaN(c)) continue; histogramData.Add(c); }

Please note: The individual CAGR values are collected in the histogramdata list.

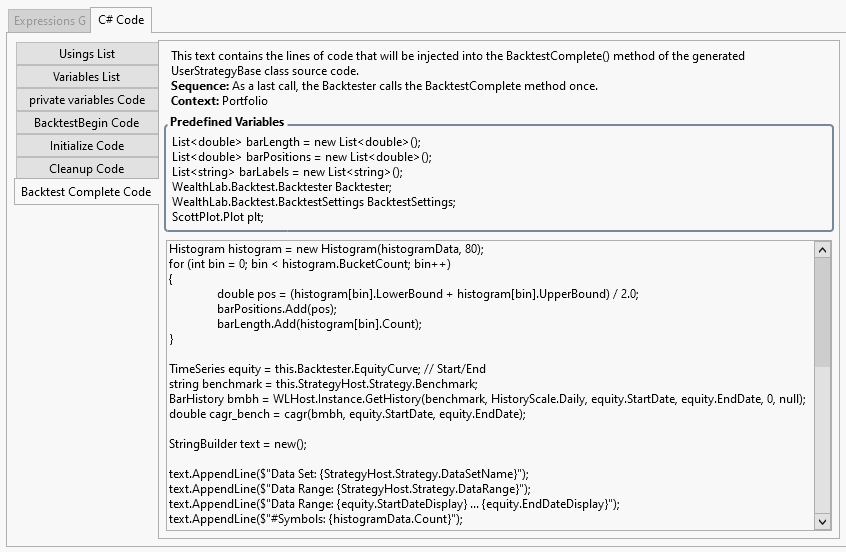

Finally we can create the histogram plot:

We want to show the CAGR of the benchmark symbol. This is calculated with the following code:

In order to make the plot more understandable we add some vertical lines and annotations:

The latter code snippets go to the "Backtest Complete Code" section:

At this stage the generation of the plot is complete. We save everything to a "PlotSpec" using the File->Save Plot Specs action.

CODE:

Histogram histogram = new Histogram(histogramData, 80); for (int bin = 0; bin < histogram.BucketCount; bin++) { double pos = (histogram[bin].LowerBound + histogram[bin].UpperBound) / 2.0; barPositions.Add(pos); barLength.Add(histogram[bin].Count); }

We want to show the CAGR of the benchmark symbol. This is calculated with the following code:

CODE:

TimeSeries equity = this.Backtester.EquityCurve; // Start/End string benchmark = this.StrategyHost.Strategy.Benchmark; BarHistory bmbh = WLHost.Instance.GetHistory(benchmark, HistoryScale.Daily, equity.StartDate, equity.EndDate, 0, null); double cagr_bench = cagr(bmbh, equity.StartDate, equity.EndDate);

In order to make the plot more understandable we add some vertical lines and annotations:

CODE:

StringBuilder text = new(); text.AppendLine($"Data Set: {StrategyHost.Strategy.DataSetName}"); text.AppendLine($"Data Range: {StrategyHost.Strategy.DataRange}"); text.AppendLine($"Data Range: {equity.StartDateDisplay} ... {equity.EndDateDisplay}"); text.AppendLine($"#Symbols: {histogramData.Count}"); // Mean double mean = histogramData.Mean(); plt.AddVerticalLine(mean , Color.Blue, 2, ScottPlot.LineStyle.Solid, "Mean"); text.AppendLine($"Mean={mean:F2} (blue)"); // Median double median= ((IEnumerable<double>)histogramData).Median(); plt.AddVerticalLine(median, Color.Orange, 2, ScottPlot.LineStyle.Solid, "Median"); text.AppendLine($"Median={median:F2} (orange)"); // Benchmark plt.AddVerticalLine(cagr_bench, Color.Red, 2, ScottPlot.LineStyle.Solid, "Benchmark"); text.AppendLine($"{benchmark}={cagr_bench:F2} (red)"); var an = plt.AddAnnotation(text.ToString(), Alignment.UpperLeft); an.MarginX = 20; an.MarginY = 20; an.Font.Size = 16; an.Shadow = false; an.BackgroundColor = Color.LightBlue;

The latter code snippets go to the "Backtest Complete Code" section:

At this stage the generation of the plot is complete. We save everything to a "PlotSpec" using the File->Save Plot Specs action.

Bravo!!

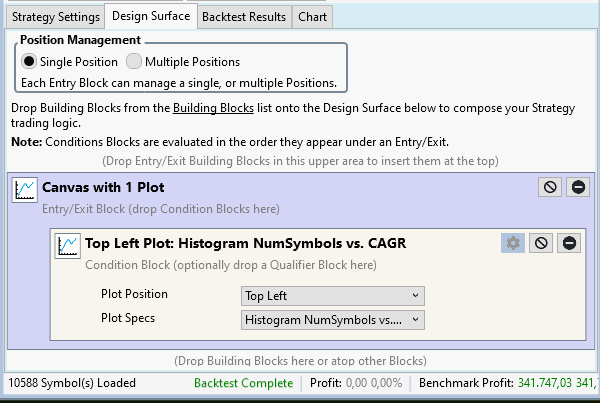

The InteractiveGraphics extension is designed to work with any Building Block Strategy.

In addition to the stratgy's building blocks a "Canvas" block is added along with sole "Plot" blocks inside the canvas.

For the "#Symbols vs. CAGR" we need no trading strategy building blocks. The complete stratgy consists of the "Canvas" building block and its internal "Plot" block alone:

Please note how we selected the PlotSpec generated above in the "Plot" building block.

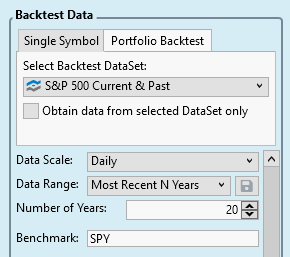

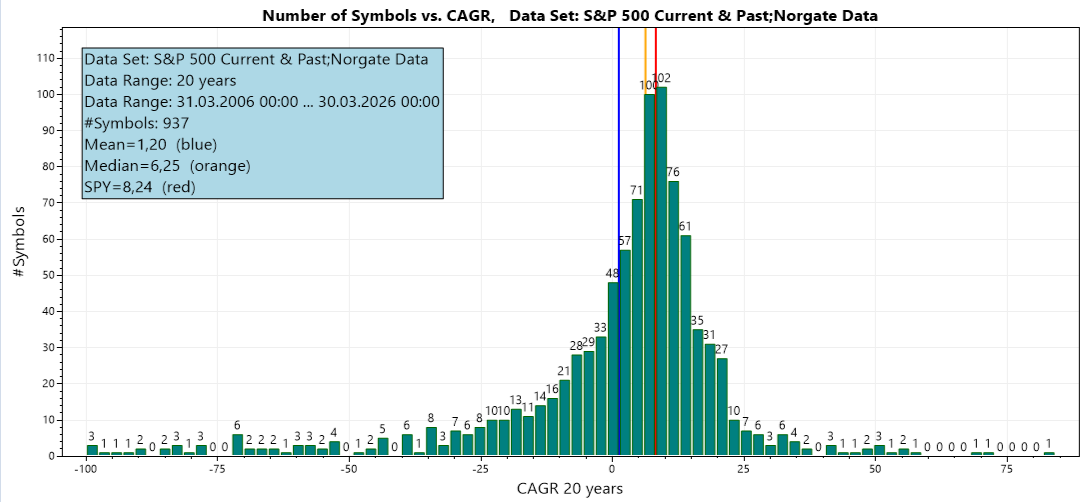

Now everything is in place and we can produce "#Symbols vs. CAGR" plots for arbitrary Data Sets and Data Ranges. As an example I used the S&P 500 and 20 years:

That reults in this beautiful graphic:

In addition to the stratgy's building blocks a "Canvas" block is added along with sole "Plot" blocks inside the canvas.

For the "#Symbols vs. CAGR" we need no trading strategy building blocks. The complete stratgy consists of the "Canvas" building block and its internal "Plot" block alone:

Please note how we selected the PlotSpec generated above in the "Plot" building block.

Now everything is in place and we can produce "#Symbols vs. CAGR" plots for arbitrary Data Sets and Data Ranges. As an example I used the S&P 500 and 20 years:

That reults in this beautiful graphic:

Your Response

Post

Edit Post

Login is required