I have been back-testing an academic paper that examines the relations between the MOVE index and the VIX. The code below is certainly not a strategy that is tradeable but it seems to show that there is information contained in the MOVE / VIX ratio that could be incorporated in other trading strategies.

Source papers:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5001821

https://alphainacademia.substack.com/p/a-strategy-for-the-post-pandemic

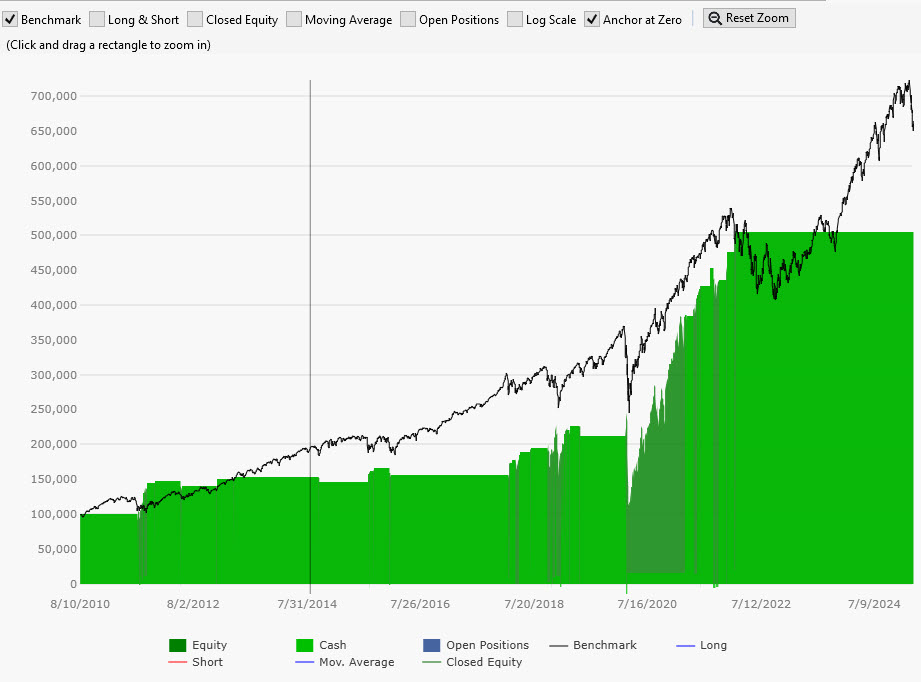

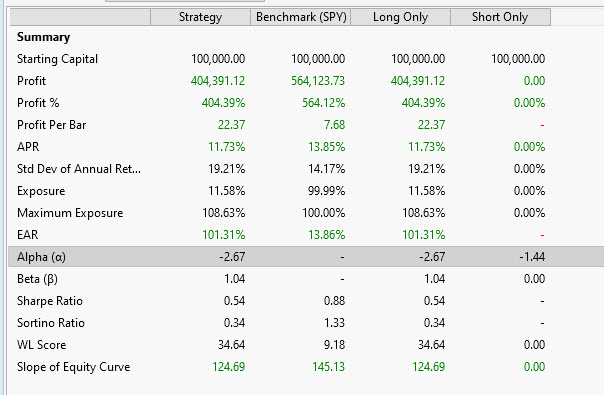

I have deviated from the original paper which used a linear fit between MOVE and VIX and used the residuals as a signal. The strategy below uses the ratio of MOVE/VIX and purchases at low values of the ratio. This could be interpreted as situations where equity markets are over-reacting compared to bond markets.

I used SPXL as the underlying and used yahoo data for MOVE and VIX. ( MOVE data is from CBOE but WL does not have it added).

Source papers:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5001821

https://alphainacademia.substack.com/p/a-strategy-for-the-post-pandemic

I have deviated from the original paper which used a linear fit between MOVE and VIX and used the residuals as a signal. The strategy below uses the ratio of MOVE/VIX and purchases at low values of the ratio. This could be interpreted as situations where equity markets are over-reacting compared to bond markets.

I used SPXL as the underlying and used yahoo data for MOVE and VIX. ( MOVE data is from CBOE but WL does not have it added).

CODE:

// Use the ratio of MOVE to VIX to determine corret timing for long entry. // <a href="https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5001821" target="_blank">https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5001821</a> // <a href="https://alphainacademia.substack.com/p/a-strategy-for-the-post-pandemic" target="_blank">https://alphainacademia.substack.com/p/a-strategy-for-the-post-pandemic</a> using WealthLab.Backtest; using System; using WealthLab.Core; using System.Linq; namespace WealthScript14 { public class DFG : UserStrategyBase { string VIX = "^VIX", MOVE = "^MOVE"; BarHistory MOVE_bars, VIX_bars; int MAPeriod = 100; double Threshold , VIX_Upper; TimeSeries close1, close2, ActualRatio, ActualRatioSMA, Delta; public DFG() : base() { AddParameter("Threshold", ParameterType.Double, 3.0, 1.0, 6.0, 0.5); } public override void Initialize(BarHistory bars) { VIX_bars = GetPairHistory(bars, VIX); MOVE_bars = GetPairHistory(bars, MOVE); Threshold = Parameters[0].AsDouble; ActualRatio = MOVE_bars.Close / VIX_bars.Close; PlotTimeSeries(ActualRatio, "Ratio " + MOVE + "/" + VIX, "RatioPane", WLColor.Navy); StartIndex = MAPeriod; } public override void Execute(BarHistory bars, int idx) { if ( GetPositions().Where(p => p.IsOpen == true).Count() == 0 && ActualRatio[idx] < Threshold ) { PlaceTrade(bars, TransactionType.Buy, OrderType.Market, 0, "Buy" ); } else if (ActualRatio[idx] > Threshold ) { PlaceTrade(bars, TransactionType.Sell, OrderType.Market, 0, "Sell" ); } } } }

Rename

Currently there are no replies yet. Please check back later.

Your Response

Post

Edit Post

Login is required