finantic.Optimizer

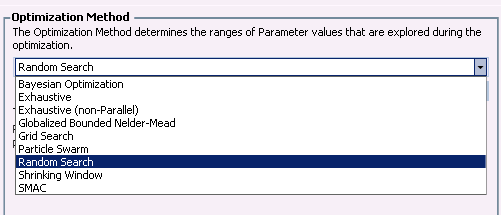

The finantic.Optimizer Extension contains sveral advanced optimizer algorithms:

Random Search

Random search optimizer initializes random parameters between min and max of the provided parameters.

Grid Search

Simple grid search that tries all combinations of the provided parameters.

Particle Swarm

Particle Swarm optimizer (PSO). PSO is initialized with a group of random particles and then searches for optima by updating generations. In every iteration, each particle is updated by following two „best“ values. The first one is the best solution found by the specific particle so far. The other „best“ value is the global best value obtained by any particle in the population so far.

Globalized Bounded Nelder-Mead

Globalized bounded Nelder-Mead method. This version of Nelder-Mead optimization avoids some of the shortcomings the standard implementation. Specifically it is better suited for multi-modal optimization problems through its restart property. It also respect the bounds given by the provided parameter space.

Bayesian Optimization

Bayesian optimization (BO) for global black box optimization problems. BO learns a model based on the initial parameter sets and scores. This model is used to sample new promising parameter candidates which are evaluated and added to the existing parameter sets. This process iterates several times. The method is computational expensive so is most relevant for expensive problems, where each evaluation of the function to minimize takes a long time, like hyper parameter tuning a machine learning method. But in that case it can usually reduce the number of iterations required to reach a good solution compared to less sophisticated methods.

SMAC: Sequential Model-Based Optimization for General Algorithm Configuration

Implementation of the SMAC algorithm. This approach constructs explicit regression models to describe the dependence of target algorithm performance on parameter settings. This paradigm is extended to general algorithm configuration problems, allowing many categorical parameters and optimization for sets of instances. SMAC selects configurations based on a model rather than uniformly at random.

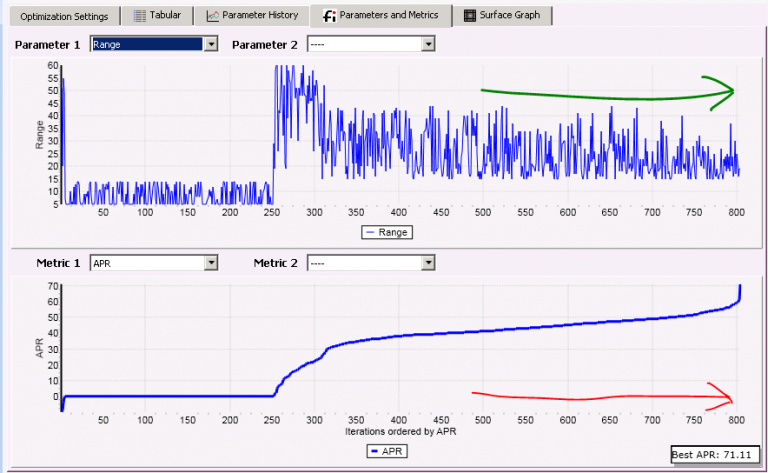

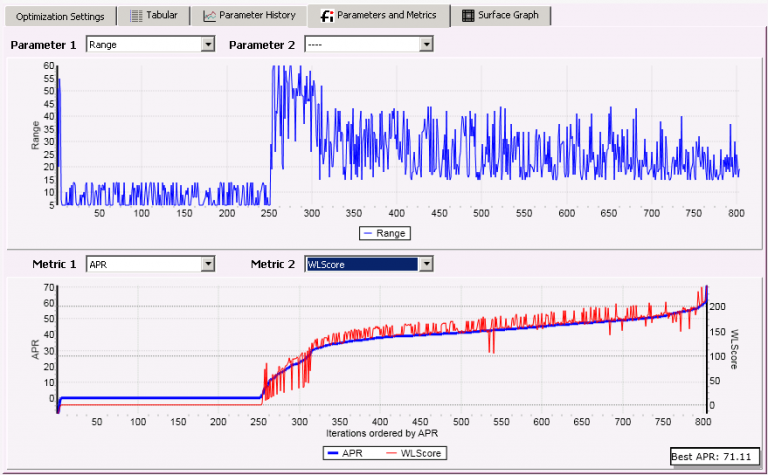

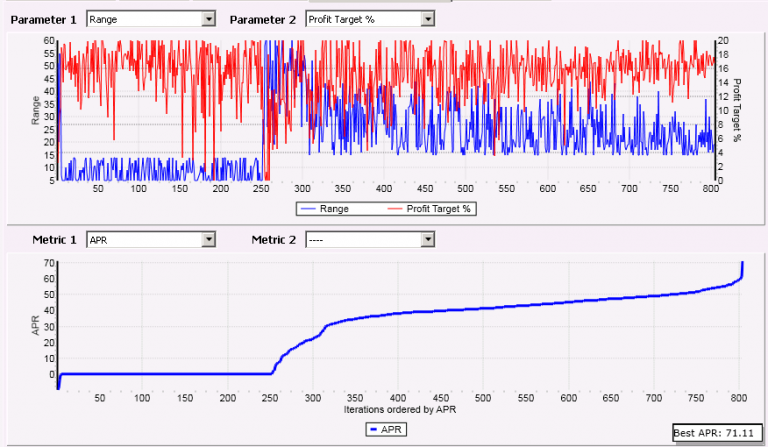

Parameters and Metrics

Parameters and Metrics is an Optimization Visualizer Exrension for WealthLab 8. It shows two simple yet powerful graphs which let you understand and interpret the results of an optimization run even if many parameters are involved.

Basic Idea behind the Graphs

The optimizer algorithm uses various parameter combinations as it walks towards an optimal value for it’s target metric. The charts display this walk to the optimum. (Everything is ordered by the target metric) when we go more to the right in the chart, we come closer to our goal: The best value for the target metric.

The „Parameter“ pane shows the parameter values tried and used along this way. It may display this history of parameter values, for all parameters, one by one.

How does it work?

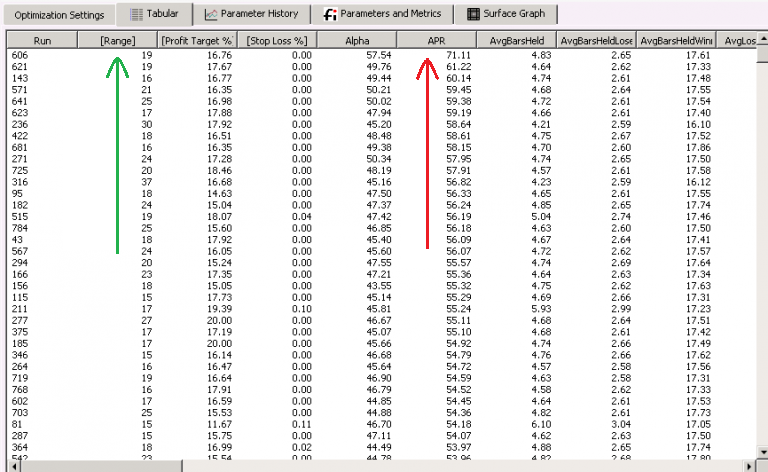

The graphs are best explained starting with the Tabular result view of an optimization run in WL8, see the Screenshots view for more information.

Screenshots

Change Log

- Removed logging, which caused trouble with very large optimizations.

- Help pages improved.

- Adapt to change in WL8 framework.

- Adapted to changes in Build 77 (.Net Verion, TeeChart Version).

- Fixed issues with Correlation and Parameter Importance (missing MathNet DLL).

- Adapted to changes in WL framework.

- C:\temp no longer required.

- Run parallel option for SMAC optimizer.

- Better defaults for SMAC optimizer.

- New MostAuspiciousRun WFO Result Selector.

- First release for WealthLab8 support.

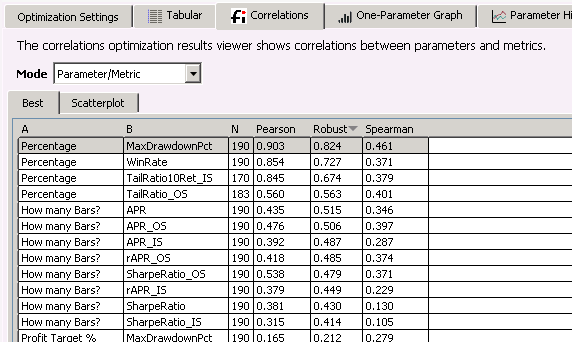

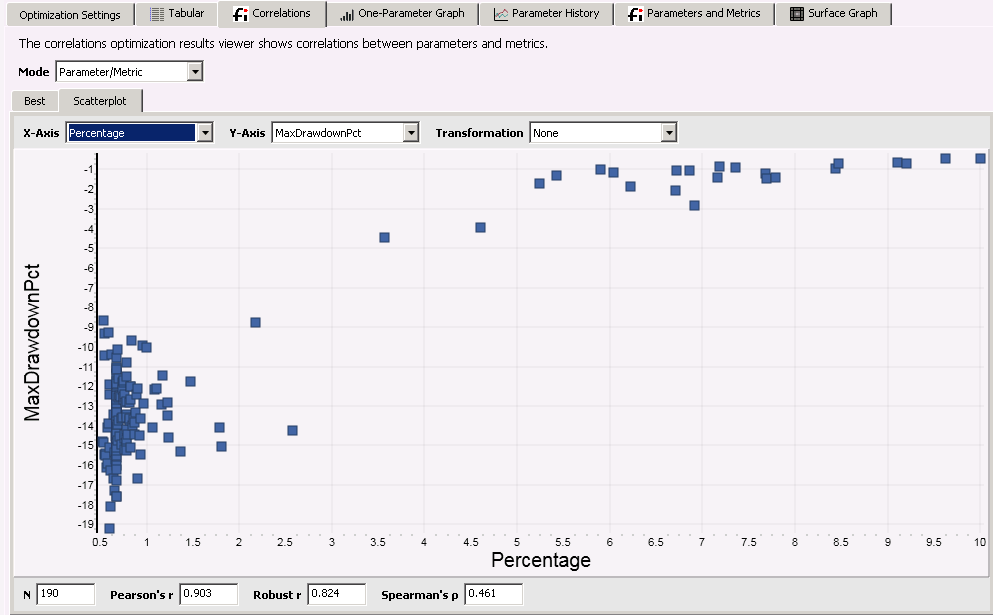

- Correlations Optimization Result Visualizer.

- Correlations calculate innovative robust r correlation: Pearsons(B2N(series)).

- Bayesian: Bugfix for ""object reference not setto an instance of an object" Exception.

- A Splitter control in Visualizer Parameters/Metrics allows resizing the graphs.

- Support for Save/Load of Optimization Results.

- Changes to adapt to new API for WL7 Build 30.

- Fixed a bug that occurs if not all Parameters are enabled for optimization.

- Added "1Y" Checkbox: use 1 Y-Axis for both curves.

- Fixed margins for Graphics and Axis.

- GridSearch: better parameter choices if 1 or two steps for this parameter (default, 1/3, 2/3).

- Changes required to work with some new features of the WL7 Optimization.

- Fixed issues related to empty metrics in drop down box.

- Better error handling.

- Better defaults in OptResultViewer "Parameters and Metrics".

- Minor Bug Fixes.

- Minor bug fixes.

- Adapted to some changed in WL7.

- Baseline release.