Backtest and Auto-Trade OptionsPublished: 6/21/2023

Updated: 2/12/2025

|

|

This article assumes a solid understanding of options and backtesting with C# Coded strategies. If you are new to options, we recommend familiarizing yourself with the basics before delving into the intricacies of programming option strategies in WealthLab. For seasoned options traders looking to enhance their trading arsenal, this article provides a valuable resource to further refine and optimize their approach.

Disclaimer!

The examples on this page are not recommended strategies and serve only as informational examples for your own strategy code.

Backtesting with Synthetic Option Pricing

You can create option trading strategies without historical option data using OptionSynthetic static class methods. The term synthetic indicates that the option prices are synthesized using a Black-Scholes option model. Prices generated from the model do not represent actual market prices, but can be representative for the purpose of backtesting and developing live trading strategies.

Futures Mode Required

For backtests to report the correct profit for option trades, Futures Mode must be enabled in Preferences (F12) > Backtest > Other Settings.

I recommend leaving Futures Mode enabled. The only time you might need to turn it off is to backtest stock symbols that match a futures symbol in "Markets & Symbols", which can happen when using wildcards for futures symbols.

Also note that it's not required to enter option symbols in Markets & Symbols for U.S. options returned by one of the integrated option data/broker providers.

GetOptionsSymbol

OptionSynthetic.GetOptionsSymbol() facilitates identifying contract(s) by right, strike, and expiration in a WealthLab strategy. For more parameter details, see GetOptionSymbol in the Live Option Pricing section later in this article.

Since synthetic options work without option chains, OptionSynthetic.GetOptionsSymbol() returns strike prices in various increments depending on the underlier price as follows:

| Price | Strike Increment |

|---|---|

| Above $1000 | $25 |

| >= $200 | $10 |

| >= $10 | $5 |

| Below $10 | $1 |

The expiration is identified using a combination of the *currentDate*, *minDaysAhead*, *useWeeklies*, and *allowExpired* parameters. Specifically, the next expiration at least *minDaysAhead* after the *currentDate* is returned. If *useWeeklies* is false, only regular monthly expirations are considered, otherwise only the non-monthly expirations are returned.

Use the symbol returned by GetOptionsSymbol() in a GetHistory() statement to obtain an option contract's price series.

GetHistory

OptionSynthetic.GetHistory() generates BarHistory objects for specified option contracts using the Black-Scholes option model to create option pricing based on the underlying stock's (or futures') BarHistory and Implied Volatility, IV.

Without live option (and underlying) prices, option traders understand that it's impossible to calculate IV that would match a live option contract's IV. Consequently, for synthetic option pricing we use a "best guess" constant IV (a value between 0.2 and 0.3 often works well for non-volatile periods). Another way is to use a varying estimate based on HV.Series() / 100.0, the Historical Volatility indicator, divided by 100.

In the chart below, you'll see Bar Histories for the stock underlier TTD (top pane), real option pricing based on the bid/ask midpoint (middle pane), and synthetic option pricing based on the known Implied Volatility on the last bar of the chart (lower pane). Prices often match within $0.05!

Example 1 - Call Option Trading on Underlier Signals

The example below demonstrates how to identify, create, and trade a synthetic option contract for an expiration at least 3 days in the future based on signals (moving average crossovers) in the underlying. When the underlier's fast moving average crosses above its slow average, one call is purchased. The call position is sold at the close of expiration or when the moving averages cross in the opposite direction.

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

namespace WealthScript9

{

public class SyntheticOptionBacktest : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

StartIndex = 40;

_sma2 = SMA.Series(bars.Close, StartIndex);

_sma1 = SMA.Series(bars.Close, 20);

PlotIndicator(_sma1);

PlotIndicator(_sma2, WLColor.Red);

}

public override void Execute(BarHistory bars, int idx)

{

Position opt = FindOpenPositionAllSymbols(_hash);

if (opt == null)

{

if (_sma1.CrossesOver(_sma2, idx))

{

// identify an option contract symbol

string osym = OptionSynthetic.GetOptionsSymbol(bars, OptionType.Call, bars.Close[idx], bars.DateTimes[idx], 3, allowExpired: true);

_hash = Math.Abs(osym.GetHashCode());

//get the option bars

_obars = OptionSynthetic.GetHistory(bars, osym, 0.4);

_syms.Add(osym);

_expiry = OptionsHelper.SymbolExpiry(osym);

// buy 1 contract

Transaction t = PlaceTrade(_obars, TransactionType.Buy, OrderType.Market, 0, _hash, "option Buy");

t.Quantity = 1;

}

}

else

{

// close the position at expiry

if (bars.DateTimes[idx].AddDays(1) >= _expiry)

ClosePosition(opt, OrderType.MarketClose, 0, "Expired");

// .. or when the underlier crosses

if (_sma1.CrossesUnder(_sma2, idx))

ClosePosition(opt, OrderType.Market);

}

}

// section is optional. Double click trades in the Positions to plot them with their BarHistory

public override void Cleanup(BarHistory bars)

{

// don't overload the chart with panes - plot only the last 5 contracts that were traded in Single Symbol Mode

if (!Backtester.Strategy.SingleSymbolMode)

return;

// Indicate the trades

foreach (Position p in GetPositionsAllSymbols())

{

if (p.Bars == bars || _syms.IndexOf(p.Symbol) < _syms.Count - 5)

continue;

PlotBarHistory(p.Bars, p.Symbol);

if (!p.NSF)

{

if (p.EntryBar > 0)

DrawTextVAlign("▲", p.EntryBar, p.Bars.Low[p.EntryBar] * 0.95, VerticalAlignment.Top, WLColor.NeonBlue, 16, 0, 0, p.Symbol, true);

if (p.ExitBar > 0)

DrawTextVAlign("▼", p.ExitBar, p.Bars.High[p.ExitBar] * 1.05, VerticalAlignment.Bottom, WLColor.NeonFuschia, 16, 0, 0, p.Symbol, true);

}

}

}

double _strike;

DateTime _expiry;

BarHistory _obars; // the option's BarHistory

SMA _sma1;

SMA _sma2;

TimeSeries _iv; // implied volatility estimate

int _hash = -1;

UniqueList<string> _syms = new UniqueList<string>();

}

}

Example 2 - Sell Covered Calls

Covered call option strategies involve buying/holding shares of the underlier and selling a short call for each 100 shares owned when the market outlook is neutral or possibly bearish. Trading risk for only the short call position is theoretically infinite, but the short call option is "covered" by the underlying shares, which can be delivered/sold to the call buyer at the strike price.

No matter how high (or low) the shares trade, the call seller stands only to gain the premium collected for the selling the call option(s) plus any stock gain from the purchase price up to the strike price.

The Covered Call strategy programmed below buys the underlier on a "golden cross" signal and sells the shares on the opposite signal. On the signal to buy the underlying shares, call options are sold short. Call position(s) are closed on the expiration date or when the underlier position is sold. If the underlier position is still open at call expiration, the next contract out is sold to open a new covered call positions.

For the backtest, we select ATM (at-the-money) calls that have an expiration at least 28 days and specify to allowExpired contracts.

Finally note that the same value is assigned to both the underlying and option contract's Transaction.Weight. The helps to ensure, but doesn't guarantee, that both Positions are put added in a Portfolio backtest. Otherwise, when buying power is limited, portfolio positions are processed randomly and you could wind up with stock and no options or even worse - uncovered short calls!

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

namespace WealthScript4

{

public class CoveredCalls : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

StartIndex = 200;

_sma2 = SMA.Series(bars.Close, StartIndex);

_sma1 = SMA.Series(bars.Close, 50);

PlotIndicator(_sma1);

PlotIndicator(_sma2, WLColor.Red);

// use RSI for Transaction.Weight

_rsi = RSI.Series(bars.Close, 14);

}

public override void Execute(BarHistory bars, int idx)

{

Position p = FindOpenPosition(1); // reference to underlying position, if exists

bool exitNextBar = false;

// underlying strategy

if (!HasOpenPosition(bars, PositionType.Long))

{

if (_sma1.CrossesOver(_sma2, idx))

{

// buy 200 shrs underlying

Transaction t1 = PlaceTrade(bars, TransactionType.Buy, OrderType.Market, 0, 1, "Buy underlier");

t1.Quantity = 200;

t1.Weight = _rsi[idx];

// covered call strategy: if holding the underlying, sell call(s) when price closes below the fast moving avg

// the synthetic option symbol with at least 28 days to expiration

ShortACall(bars, idx, t1.Quantity, bars.Close[idx]);

}

}

else

{

if (_sma1.CrossesUnder(_sma2, idx))

{

exitNextBar = true;

ClosePosition(p, OrderType.Market);

}

// take care of the call option too

Position opt = FindOpenPositionAllSymbols(_hash);

if (opt != null)

{

// close the position at expiry

if (bars.DateTimes[idx].AddDays(1) >= _expiry)

ClosePosition(opt, OrderType.Market, 0, "Expired");

// .. or when the underlier is sold

if (exitNextBar)

ClosePosition(opt, OrderType.Market);

}

else if (!exitNextBar)

{

// short another ATM call - at the entry price or higher

ShortACall(bars, idx, p.Quantity, p.EntryPrice);

}

}

}

private Transaction ShortACall(BarHistory bars, int idx, double underlierShares, double minStrike)

{

_osym = OptionSynthetic.GetOptionsSymbol(bars, OptionType.Call, minStrike, bars.DateTimes[idx], 28, allowExpired: true);

_hash = Math.Abs(_osym.GetHashCode());

_expiry = OptionsHelper.SymbolExpiry(_osym);

//get the synthetic option bars using a nominal IV

_obars = OptionSynthetic.GetHistory(bars, _osym, 0.28);

_syms.Add(_obars.Symbol);

// short 1 call per 100 shares owned (covered calls)

Transaction t2 = PlaceTrade(_obars, TransactionType.Short, OrderType.Market, 0, _hash, "short calls");

t2.Quantity = Math.Floor(underlierShares / 100);

t2.Weight = _rsi[idx];

return t2;

}

// section is optional. Double click trades in the Positions to plot them with their BarHistory

public override void Cleanup(BarHistory bars)

{

// don't overload the chart with panes - plot only the last 5 contracts that were traded in Single Symbol Mode

if (!Backtester.Strategy.SingleSymbolMode)

return;

// Indicate the trades

foreach (Position p in GetPositionsAllSymbols())

{

if (p.Bars == bars || _syms.IndexOf(p.Symbol) < _syms.Count - 5)

continue;

PlotBarHistory(p.Bars, p.Symbol);

if (!p.NSF)

{

if (p.EntryBar > 0)

DrawTextVAlign("▲", p.EntryBar, p.Bars.Low[p.EntryBar] * 0.95, VerticalAlignment.Top, WLColor.NeonBlue, 16, 0, 0, p.Symbol, true);

if (p.ExitBar > 0)

DrawTextVAlign("▼", p.ExitBar, p.Bars.High[p.ExitBar] * 1.05, VerticalAlignment.Bottom, WLColor.NeonFuschia, 16, 0, 0, p.Symbol, true);

}

}

}

string _osym;

DateTime _expiry;

BarHistory _obars; // the option's BarHistory

SMA _sma1;

SMA _sma2;

int _hash = -1;

UniqueList<string> _syms = new UniqueList<string>();

RSI _rsi;

}

}

Live Option Pricing and Trading

Currently, the following WealthLab-integrated providers support all or some features for option chains, historical data for non-expired contracts, and option trading:

- Interactive Brokers

- Schwab

- Alpaca

- Tradier (has expired daily contract data approximately 10 years back)

- IQFeed (data only)

Of these, Interactive Brokers probably has the largest user base at WealthLab, so we'll use examples targeting the IBHistorical.Instance. It's important to know Interactive Brokers, or IB, supports only intraday data for options. Check the Provider's Help docs for specific examples.

Always consider the following when setting up Interactive Brokers for testing and trading options:

- Intraday (only) - you must have data permissions for both instruments - options and underlying contracts.

- Interval - shorter intervals increase the time required collect data

- Data Range - long data ranges greatly increase the time required collect data

- What to Request - Since option trade data tends to be illiquid, Bid/Ask MidPoint is a better representation of option pricing through the day. Select it in WealthLab's IB Configuration.

GetOptionsSymbol()

Option Symbol Format

Each data provider has its own option symbol format that is returned by GetOptionsSymbol(). Similar to the synthetic method for GetOptionsSymbol(), specify parameters as required for the desired contract. The provider will automatically find a corresponding option symbol from the option chain.

public virtual string GetOptionsSymbol(BarHistory underlierBars, OptionType optionType, double price, DateTime currentDate, int minDaysAhead = 0, bool useWeeklies = false, bool allowExpired = false, bool closestStrike = true, double multiplier = 100)

Let's go over the parameters and what they mean:

| Parameter | Description |

|---|---|

| underlierBars | Pass the BarHistory reference (bars) of the underlier for symbol and scale information. |

| optionType | OptionType is a public enum OptionType { Call, Put }; |

| price | The price should be near the desired strike. To find a strike that's 20% higher than the current price, multiply by 1.2. You don't need to specify the exact strike price. See closestStrike below. |

| currentDate | Pass the current date of the backtest for this parameter and use the next 3 parameters to identify the desired expiration. |

| minDaysAhead | This sets the minimum number of days allowed to expiration from the currentDate parameter. For example, if currentDate = 14 June and minDaysAhead = 5, an expiration on or after 19 June be selected. |

| useWeeklies | useWeeklies must be false to return regular [monthly] expirations. Otherwise, only contracts with weekly expirations will be returned, which do not include regular expirations. |

| allowExpired | Backtesting using expired contract data is possible with data that you downloaded while the contract was trading. However, since option chains are available only for non-expired contracts, you must set allowExpired to true to identify past expirations. Set allowExpired to false for live trading. |

| closestStrike | true finds the strike closest to price for both Calls and Puts; false finds the next strike higher than price for a Call, or the next strike lower than price for a Put. |

| multiplier | If there's a need to identify a contract with a multiplier different than 100, specify it here. |

Example 3 - Plot At-The-Money Call

The following script uses GetOptionsSymbol() to find the contract from an option chain with the following properties:

- Call is specified using OptionType.Call

- Strike price closest to the last bar's closing price

- Expiration - not weeklies, regular only

- And, the expiry must be at least 10 days in the future

Data Providers access the Option Chain behind the scenes to return the most appropriate contract symbol as a string in the optSym variable, which you can use to GetHistory() from the provider.

Because IB only returns intraday options data, note how the script checks the scale of the underlier's chart bars. If the scale is intraday, use GetHistory() for the option symbol just as you would for any secondary symbol request. But, if the bars are Daily, the code shows how to access 30-minute bars for the previous 12 months, scale them to Daily bars, and finally synchronize with the Daily chart bars. You can reuse this programming pattern.

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

using WealthLab.InteractiveBrokers;

namespace WealthScript1

{

public class ATMOption : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

double price = bars.Close[bars.Count - 1];

DateTime currentDate = bars.DateTimes[bars.Count - 1];

int minDaysToExpiry = 10;

bool weeklies = false;

bool closestStrike = true;

bool allowExpired = false;

string optSym = IBHistorical.Instance.GetOptionsSymbol(bars, OptionType.Call, price, currentDate, minDaysToExpiry, weeklies, allowExpired, closestStrike);

DrawHeaderText("ATM Call: " + optSym, WLColor.NeonGreen, 14);

if (bars.Scale.IsIntraday)

{

_obars = GetHistory(bars, optSym);

}

else // Daily+

{

// get all the 30min option data from IB

_obars = GetHistoryUnsynched(optSym, HistoryScale.Minute30);

if (_obars == null)

{

WriteToDebugLog($"Could not get option data for {optSym}. Check the Log Viewer for more info.");

return;

}

// Compress and sync the bars

_obars = BarHistoryCompressor.ToDaily(_obars);

_obars = BarHistorySynchronizer.Synchronize(_obars, bars);

}

PlotBarHistory(_obars, optSym);

}

//execute the strategy rules here, this is executed once for each bar in the backtest history

public override void Execute(BarHistory bars, int idx)

{ }

BarHistory _obars; // the option's BarHistory

}

}

Option Greeks and IV

Passing an option symbol to a call for GetGreeks() will return a OptionGreek object, which contains values for the "greeks" and other information like Implied Volatility, IV, for the contract.

**Note! **

Data for greeks may not be available in which case

GetGreeks()will return null. Schwab, Tradier, and Alpaca have fast/excellent greek data retrieval in real time.

The next example uses code similar to the previous example to find the ATM call and put symbols, passes them to GetGreeks() and displays the result - the values of an OptionGreek object. The greeks may not be available at all times (e.g., after market hours), and it's possible to get a null result.

For best results for IB, run the example during market hours. For other brokers, like Tradier, just replace using WealthLab.InteractiveBrokers and IBHistorical.Instance with using WealthLab.Tradier and TradierHistorical.Instance.

Example 4 - GetGreeks()

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

using WealthLab.InteractiveBrokers;

namespace WealthScript2

{

public class ATMOption : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

double price = bars.Close[bars.Count - 1];

DateTime currentDate = bars.DateTimes[bars.Count - 1];

int minDaysToExpiry = 10;

bool weeklies = false;

bool closestStrike = true;

bool allowExpired = false;

// ATM Call

string optSym = IBHistorical.Instance.GetOptionsSymbol(bars, OptionType.Call, price, currentDate, minDaysToExpiry, weeklies, allowExpired, closestStrike);

OptionGreek greek = IBHistorical.Instance.GetGreeks(optSym);

DisplayTheGreeks(optSym, greek, WLColor.NeonGreen);

// ATM Put

optSym = IBHistorical.Instance.GetOptionsSymbol(bars, OptionType.Put, price, currentDate, minDaysToExpiry, weeklies, allowExpired, closestStrike);

greek = IBHistorical.Instance.GetGreeks(optSym);

DisplayTheGreeks(optSym, greek, WLColor.NeonGreen);

}

void DisplayTheGreeks(string optSym, OptionGreek greek, WLColor clr, int fontSize = 14)

{

if (greek == null)

{

DrawHeaderText(String.Format("Greeks for {0} are null", optSym), clr, 14);

return;

}

DrawHeaderText("Symbol = " + greek.Symbol, clr, 14);

DrawHeaderText("MidPoint = " + greek.OptionPrice.ToString("N2"), clr, 14);

DrawHeaderText("IV = " + greek.IV.ToString("N2"), clr, 14);

DrawHeaderText("Delta = " + greek.Delta.ToString("N2"), clr, 14);

DrawHeaderText("Gamma = " + greek.Gamma.ToString("N2"), clr, 14);

DrawHeaderText("Theta = " + greek.Theta.ToString("N2"), clr, 14);

DrawHeaderText("Vega = " + greek.Vega.ToString("N2"), clr, 14);

DrawHeaderText("Underlying = " + greek.UnderlyingPrice.ToString("N2"), clr, 14);

}

//execute the strategy rules here, this is executed once for each bar in the backtest history

public override void Execute(BarHistory bars, int idx)

{ }

BarHistory _obars; // the option's BarHistory

}

}

Calculated Option Price and IV

Interactive Brokers' API contains methods to calculate current implied volatility (IV) and option prices using Black-Scholes and the price of the underlying. To find the current IV, the option price is also required. Likewise, to calculate an option price, IV is required.

Knowing the actual IV is useful for more accurate OptionSynthetic pricing. The following example demonstrates.

Example 5 - Calculated Option Price and IV

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

using WealthLab.InteractiveBrokers;

namespace WealthScriptOptionsExample5

{

public class CalculatedGreeks : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

double price = bars.Close[bars.Count - 1];

DateTime currentDate = bars.DateTimes[bars.Count - 1];

int minDaysToExpiry = 10;

bool weeklies = false;

bool closestStrike = true;

bool allowExpired = false;

string optSym = IBHistorical.Instance.GetOptionsSymbol(bars, OptionType.Call, price, currentDate, minDaysToExpiry, weeklies, allowExpired, closestStrike);

DrawHeaderText("ATM Call: " + optSym, WLColor.NeonGreen, 14);

if (bars.Scale.IsIntraday)

{

_obars = GetHistory(bars, optSym);

}

else // assuming Daily

{

// request 30 minute bars and synchronize with the non-intraday scale

_obars = GetHistoryUnsynched(optSym, HistoryScale.Minute30);

if (_obars != null)

{

// compress to Daily bars

_obars = BarHistoryCompressor.ToDaily(_obars);

// sync the bars with the non-intraday data

_obars = BarHistorySynchronizer.Synchronize(_obars, bars);

}

}

double iv = 0;

if (_obars == null)

{

WriteToDebugLog("Could not get option data, check the Log Viewer for more info.");

return;

}

else

{

PlotBarHistory(_obars, optSym);

DrawHeaderText("Option Last Value: " + _obars.LastValue.ToString("N2"), WLColor.NeonOrange, 14);

DrawHeaderText("bars Last Value: " + bars.LastValue.ToString("N2"), WLColor.NeonOrange, 14);

//use the price of the option symbol and underlying to calculate IV

iv = IBHistorical.Instance.CalculateIV(optSym, _obars.LastValue, bars.LastValue);

DrawHeaderText("Calculated IV = " + iv.ToString("N4"), WLColor.NeonRed, 14);

}

if (iv > 0)

{

//use IV and underlying price to calculate the options price

double op = IBHistorical.Instance.CalculateOptionPrice(optSym, iv, bars.LastValue); // priceUnderlying

DrawHeaderText("Calculated Option Price = " + op.ToString("N2"), WLColor.NeonRed, 14);

//use IV to create the synthetic contract - compare it to the live prices

BarHistory osynth = OptionSynthetic.GetHistory(bars, "!" + optSym, iv);

PlotBarHistory(osynth, optSym, WLColor.Cyan);

}

}

//execute the strategy rules here, this is executed once for each bar in the backtest history

public override void Execute(BarHistory bars, int idx)

{ }

BarHistory _obars; // the option's BarHistory

}

}

Long Straddle Strategy

While a Long Straddle itself isn't news, the way it's implemented in the strategy below is novel.

A long straddle options strategy simultaneously holds long positions for calls and puts at the same strike price and expiration. If the stock makes a big move in either direction, this market neutral option combination produces a position that can often result in large profits.

The example code builds on WealthLab strategy programming elements above to create a Spread/Straddle Strategy Template that can be modified and reused for option spread and straddle strategy types.

A key component of the template is a method called PutOnOptionTrade(). Its arguments include TransactionType, OptionType, strike, minDaysToExpiry, etc., each of which must specify both sides of a spread/straddle trade according to the option strategy. Here are a couple of examples:

// Long Straddle, 60 days to expiration; 0 strike parameters are shortcuts specifying ATM strikes

PutOnOptionTrade(bars, idx, 60, 1, TransactionType.Buy, OptionType.Call, 0, TransactionType.Buy, OptionType.Put, 0, null);

// Bull Put Spread, 30 days to expiration

double strike1 = Math.Ceiling(bars.Close[idx] / 5) * 5;

double strike2 = strike1 - (strike1 > 100 ? 10 : 5);

PutOnOptionTrade(bars, idx, 30, 1, TransactionType.Short, OptionType.Put, strike1, TransactionType.Buy, OptionType.Put, strike2, null);

To customize the strategy, you only need to come up with the entry condition and call PutOnOptionTrade() to open a spread or straddle position. The strategy holds the positions to expiration, but the exit logic can also be modified easily - to use a profit target, for example.

Finally, the strategy template "as is" employs OptionSynthetic for options pricing using expired contracts. But by substituting a data provider instance (e.g., IBHistorical.Instance) for the last null parameter in PutOnOptionTrade(), the strategy switches to use live symbol/data when non-expired (live) contracts are specified.

Example 6 - Long Straddle Strategy (Spread and Straddle Template)

using WealthLab.Backtest;

using System;

using WealthLab.Core;

using WealthLab.Data;

using WealthLab.Indicators;

using System.Collections.Generic;

// using WealthLab.InteractiveBrokers; // IBHistorical.Instance

// using WealthLab.Tradier; // TradierHistorical.Instance

// using WealthLab.IQFeed; // IQFeedHistorical.Instance

namespace WealthScript2

{

public class OptionSpreadAndStrangleWrapper : UserStrategyBase

{

public override void Initialize(BarHistory bars)

{

StartIndex = 21;

//set up a daily indicator using Daily bars (CMO example)

BarHistory daily = GetHistoryUnsynched(bars.Symbol, HistoryScale.Daily);

_ind = CMO.Series(daily.Close, 10);

_ind = TimeSeriesSynchronizer.Synchronize(_ind, bars);

PlotTimeSeriesLine(_ind, "CMO", "ind", WLColor.NeonBlue);

_spreadOrStrangleProfit = new TimeSeries(bars.DateTimes);

PlotTimeSeriesHistogramTwoColor(_spreadOrStrangleProfit, "Trade Profit", "SP", WLColor.LawnGreen, WLColor.OrangeRed);

}

public override void Execute(BarHistory bars, int idx)

{

Position pos1 = FindOpenPositionAllSymbols(_hash1);

Position pos2 = FindOpenPositionAllSymbols(_hash2);

DateTime dte = bars.DateTimes[idx];

if (pos1 == null && pos2 == null)

{

if (_ind.CrossesOver(50, idx)) /*** modify entry condition here ***/

{

//sample parameters for a Long Strangle: ATM Call and Put, min 60 days to expiration

PutOnOptionTrade(bars, idx, 60, 1, TransactionType.Buy, OptionType.Call, 0, TransactionType.Buy, OptionType.Put, 0, null);

}

}

else if (pos1 == null || pos1.NSF)

{

// ensure the backtest had cash to put on the pair, otherwise exit the orphan

ClosePosition(pos2, OrderType.MarketClose, 0, "Orphan1");

}

else if (pos2 == null || pos2.NSF)

{

// ensure the backtest had cash to put on the pair, otherwise exit the orphan

ClosePosition(pos1, OrderType.MarketClose, 0, "Orphan2");

}

else

{

_spreadOrStrangleProfit[idx] = pos1.ProfitAsOf(idx) + pos2.ProfitAsOf(idx);

bool exitTrade = false;

string reason = "expired";

if (_spreadOrStrangleProfit[idx] > 2000)

{

exitTrade = true;

reason = "profit";

}

// close the trade on expiration or before on some other condition

if (dte.AddDays(1) >= _expiry || exitTrade)

{

ClosePosition(pos1, OrderType.MarketClose, 0, reason);

ClosePosition(pos2, OrderType.MarketClose, 0, reason);

}

}

}

// For any spread or straddle that uses the same expiration date, pass 0 for striks to get ATM strikes

private void PutOnOptionTrade(BarHistory bars, int idx, int minDaysToExpiry, int contractsPerLeg,

TransactionType ttype1, OptionType otype1, double strike1,

TransactionType ttype2, OptionType otype2, double strike2,

DataProviderBase dpInstance = null)

{

if (contractsPerLeg < 1)

throw new InvalidOperationException("contractsPerLeg needs to be 1 or more");

DrawBarAnnotation(TextShape.ArrowDown, idx, true, WLColor.Gold, 20);

DrawBarAnnotation(TextShape.ArrowUp, idx, false, WLColor.Gold, 20);

double ATM = Math.Round(bars.Close[idx] / 5) * 5;

if (strike1 < 5) strike1 = ATM;

if (strike2 < 5) strike2 = ATM;

BarHistory obars1 = GetOptionHistory(bars, idx, otype1, strike1, minDaysToExpiry, dpInstance);

BarHistory obars2 = GetOptionHistory(bars, idx, otype2, strike2, minDaysToExpiry, dpInstance);

if (obars1 != null && obars2 != null)

{

_expiry = OptionsHelper.SymbolExpiry(obars1.Symbol);

_hash1 = Math.Abs(obars1.Symbol.GetHashCode());

Transaction t = PlaceTrade(obars1, ttype1, OrderType.Market, 0, _hash1);

t.Quantity = contractsPerLeg;

t.Weight = _ind[idx];

_hash2 = Math.Abs(obars2.Symbol.GetHashCode());

t = PlaceTrade(obars2, ttype2, OrderType.Market, 0, _hash2);

t.Quantity = contractsPerLeg;

t.Weight = _ind[idx];

}

}

// this routine is a wrapper to return synthetic bars if allowExpired is true, or live options pricing for future expirations if false

private BarHistory GetOptionHistory(BarHistory bars, int bar, OptionType optionType, double price, int minDaysToExpiry, DataProviderBase dpInstance = null)

{

bool liveTrade = dpInstance != null && bars.DateTimes[bar] > DateTime.Now.AddDays(-minDaysToExpiry);

DateTime currDte = bars.DateTimes[bar];

BarHistory obars = null;

//if allowExpired is true use OptionSynthetic, it's not a live trade

string optSym = liveTrade ? dpInstance.GetOptionsSymbol(bars, optionType, price, currDte, minDaysToExpiry)

: OptionSynthetic.GetOptionsSymbol(bars, optionType, price, currDte, minDaysToExpiry, allowExpired: true);

//create the option bars and save it to the bars cache

if (!liveTrade)

{

obars = OptionSynthetic.GetHistory(bars, optSym, _iv);

}

else if (bars.Scale.IsIntraday)

obars = GetHistory(bars, optSym);

else

{

// request 30 minute bars and synchronize with the non-intraday scale

obars = GetHistoryUnsynched(optSym, HistoryScale.Minute30);

if (obars != null)

{

// compress to Daily bars and synchronize

obars = BarHistoryCompressor.ToDaily(obars);

obars = BarHistorySynchronizer.Synchronize(obars, bars);

}

}

if (liveTrade)

PlotBarHistory(obars, obars.Symbol);

return obars;

}

DateTime _expiry;

double _iv = 0.45;

TimeSeries _ind;

TimeSeries _spreadOrStrangleProfit;

int _hash1 = -1;

int _hash2 = -1;

}

}

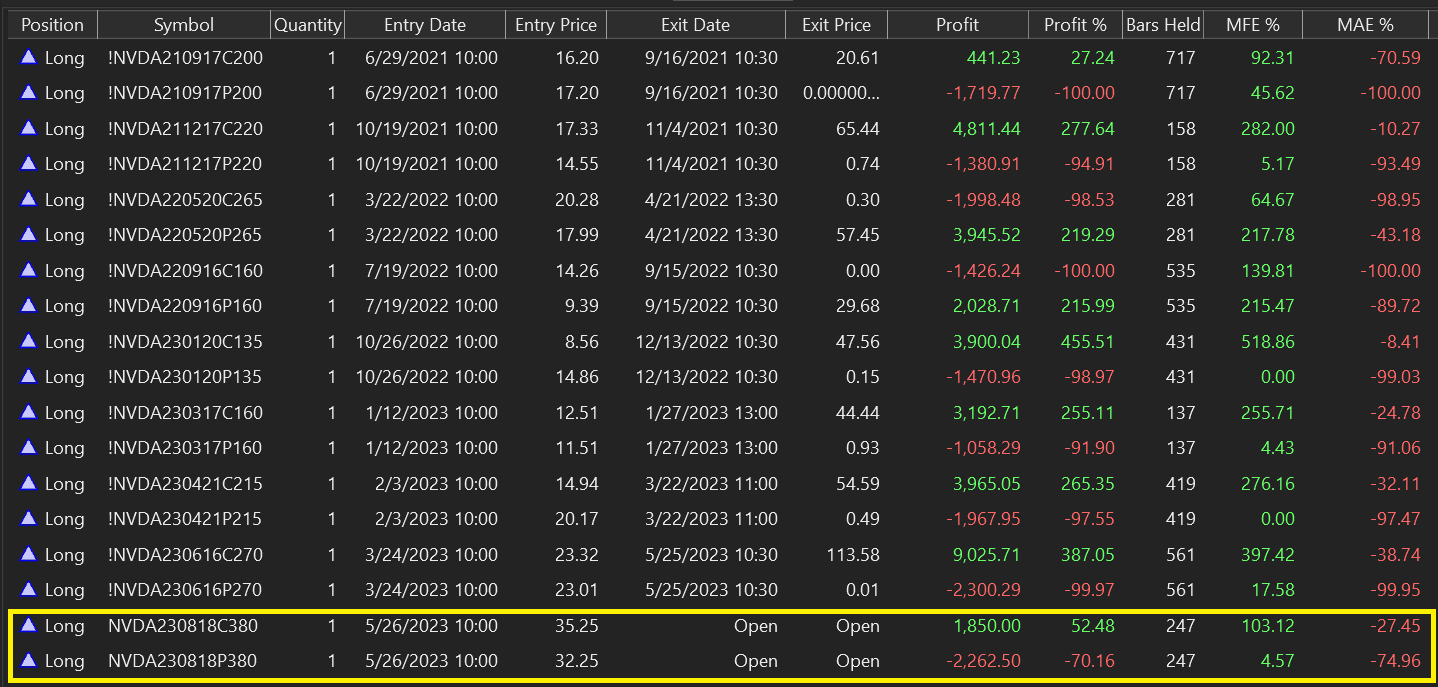

We ran the sample code on 2-years of 30-minute bars of NVDA using the IBHistorical.Instance for the final monster trade depicted in the chart below :

Note that the synthetic symbols are indicated using a "!" prefix in the Trades list. The final trade lacks the prefix because we used the IBHistorical.Instance and the strategy switched to the live contracts for the future expiration.

It never hurts to be reminded that past results are no guarantee of future returns, and admittedly we cherry-picked NVDA due to recent and typical high volatility, especially around earnings events. Nevertheless, in a short 2 years, it only took 9 NVDA long straddles to boost the account value from $10,000 to nearly $28,000.

Disclaimer!

The examples on this page are not recommended strategies and serve only as informational examples for your own strategy code.

No Credit Card required.