Hello fellows.

What do you use for filtering bad trades, thus reducing DD and increasing rate of success? I can see that even in the best swing strategies, despite being profitable, profitable rates (%) tend to be a little bit less than 50% on the lon run.

This is a post just to share ideas and experiences about what to use as a bad trades filter.

Sometimes I use a trend filter being sure that Close is avobe MA, however is too simple and has some limitations. Sometimes I use a VIX filter such as VXZ Close most be below an MA, but it looks like more ideas are necessary to have a good sort of filters to improve different strategies.

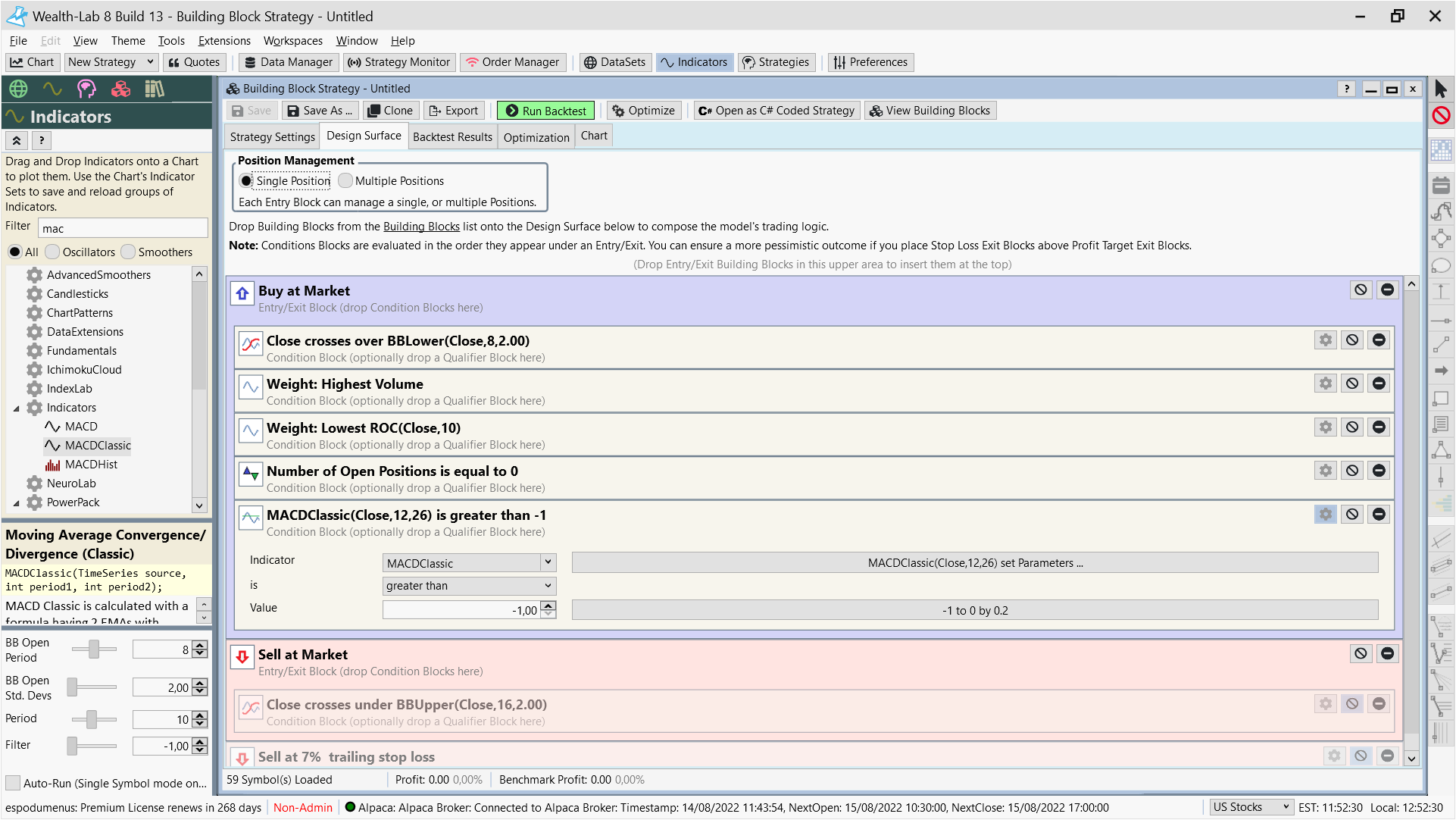

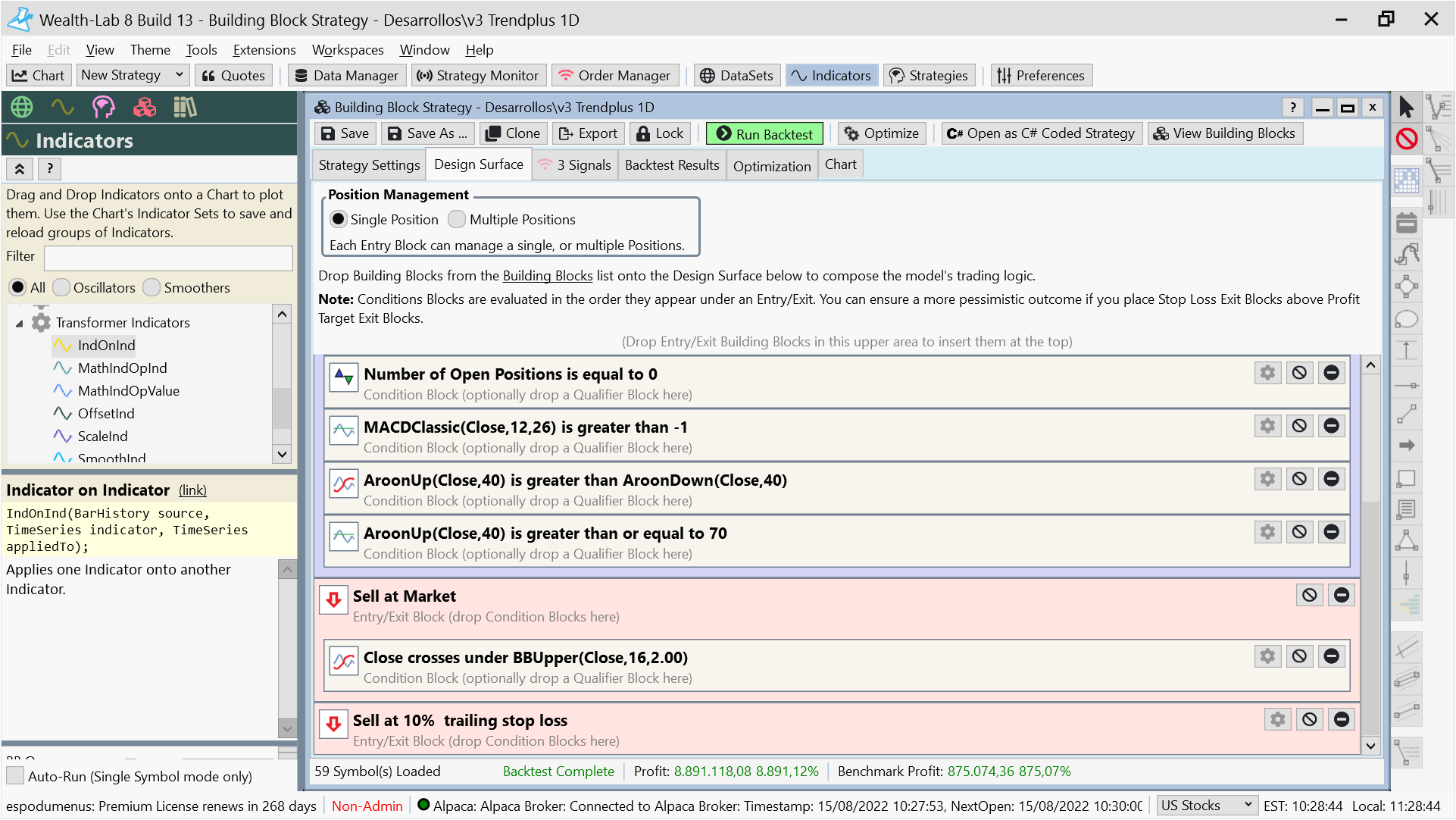

Here is an example it's intended to close on B bands too, but in order to filter positions since the very open, the strategy closes during next bar. The filter is a MACD as well as the BBLow itself.

What do you use for filtering bad trades, thus reducing DD and increasing rate of success? I can see that even in the best swing strategies, despite being profitable, profitable rates (%) tend to be a little bit less than 50% on the lon run.

This is a post just to share ideas and experiences about what to use as a bad trades filter.

Sometimes I use a trend filter being sure that Close is avobe MA, however is too simple and has some limitations. Sometimes I use a VIX filter such as VXZ Close most be below an MA, but it looks like more ideas are necessary to have a good sort of filters to improve different strategies.

Here is an example it's intended to close on B bands too, but in order to filter positions since the very open, the strategy closes during next bar. The filter is a MACD as well as the BBLow itself.

Rename

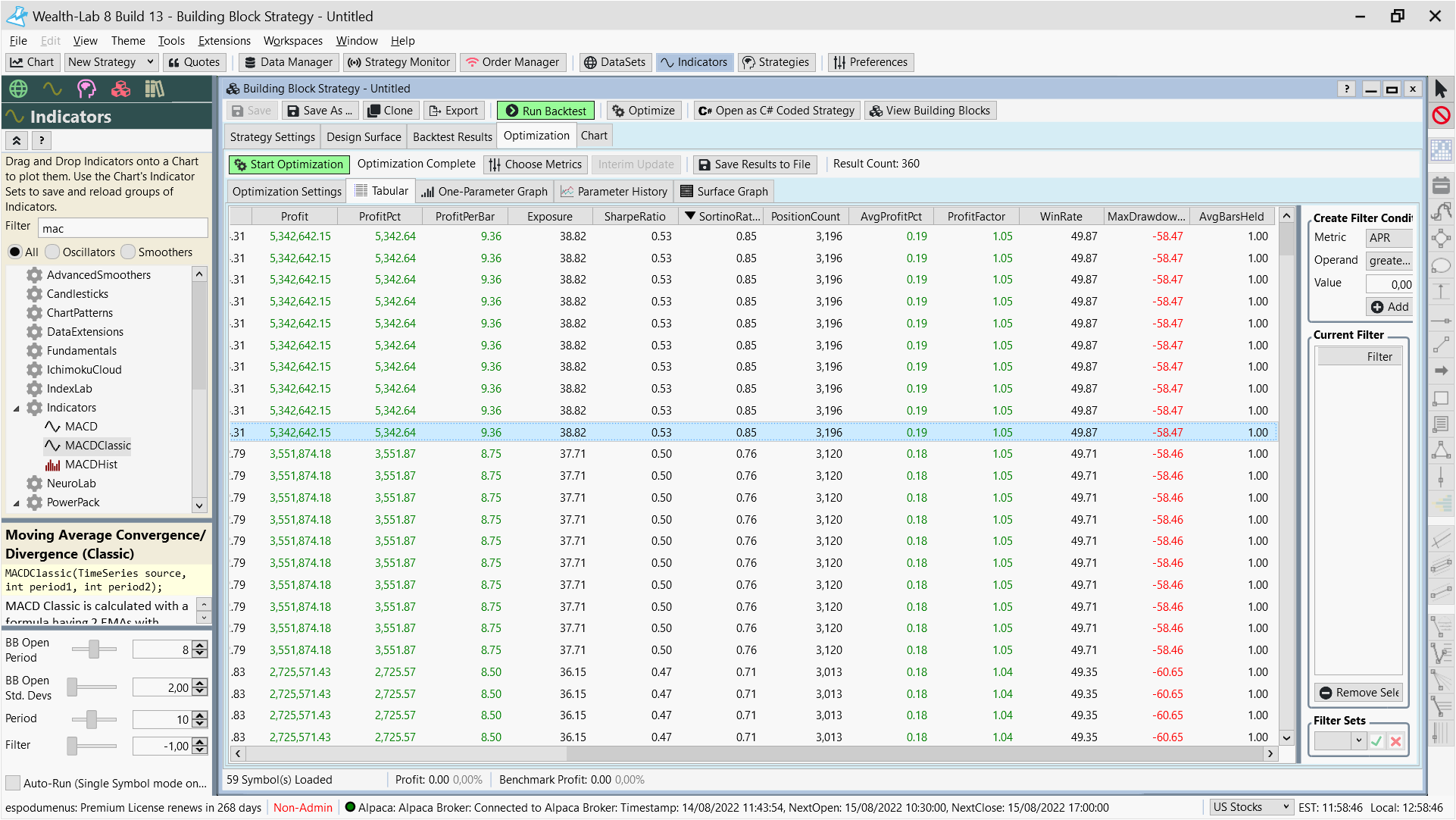

Next image is the Optimization using 30 years of data. BTW, dataset is 60 of the most traded symbols, extracted from the Nasdaq100.

The profitable positions are a little bit less than 50% and this is the best we got, DD is hughe. We need to explore additional filters option. Ideas?

The fundamental problem is that WL lacks a Performance Visualizer that separates the performance of the "Buy strategy leg" from the "Sell strategy leg" of the overall strategy. As a result, it's difficult to determine if ...

1) The strategy entered a position it should have never entered in the first place -or-

2) The strategy failed to exit a failing position soon enough.

But this discussion topic is strictly about #2, so let's concentrate on that one.

The general feeling is, if the strategy entered a "trade" (not an investment) which is not giving some immediate satisfaction, then it should be exited. That's kind of a hard pill to swallow, and perhaps that execution should be tempered with a strategy parameter the optimizer can use to temper that thinking. We want to employ an indicator that judges "How immediate?" and by "How much?" of a decline. Currently, I'm using the MACDhistogram to answer both of these questions with the threshold for selling the position being adjustable by an optimizer parameter.

I haven't looked at my Qik-exit-sell code in awhile, but I think there's even some extrapolation code in there to extrapolate to the next future bar to make this determination.

Speaking about extrapolating the future, I've always wanted to try out the Kalman filter WL extension offered by Finantic to see how well it predicts the future bar. And it will accept two inputs, so one of those inputs can be sentiment data (such as the VIX or McClellan Oscillator [from IndexLab]). If you have tried this, let us know your experiences.

1) The strategy entered a position it should have never entered in the first place -or-

2) The strategy failed to exit a failing position soon enough.

But this discussion topic is strictly about #2, so let's concentrate on that one.

The general feeling is, if the strategy entered a "trade" (not an investment) which is not giving some immediate satisfaction, then it should be exited. That's kind of a hard pill to swallow, and perhaps that execution should be tempered with a strategy parameter the optimizer can use to temper that thinking. We want to employ an indicator that judges "How immediate?" and by "How much?" of a decline. Currently, I'm using the MACDhistogram to answer both of these questions with the threshold for selling the position being adjustable by an optimizer parameter.

I haven't looked at my Qik-exit-sell code in awhile, but I think there's even some extrapolation code in there to extrapolate to the next future bar to make this determination.

Speaking about extrapolating the future, I've always wanted to try out the Kalman filter WL extension offered by Finantic to see how well it predicts the future bar. And it will accept two inputs, so one of those inputs can be sentiment data (such as the VIX or McClellan Oscillator [from IndexLab]). If you have tried this, let us know your experiences.

QUOTE:

the performance of the "Buy strategy leg" from the "Sell strategy leg"

What's are buy and sell "strategy legs" exactly?

Is there an example of the aforementioned visualizer that Wealth-Lab lacks?

After filtering ideas, there's nothing better than the Analysis Series visualizer, part of the Power Pack extension. Here's Glitch with a great explanation: https://youtu.be/7QSAyNUTe_E?t=336

QUOTE:This is exactly the leg I'd want to optimize, filtering these signals. Therefore I simplified the sell process to sell the next bar. The idea is to optimize buy signals in order to increase accuracy, then I would work on optimizing the exit strategy, in the example I provided it would be based upon B bands so when close crosses below lower bands (or alternatively a TEMA or anything between BBlower and BBupper, as a conservative approach, or a trailing SL) it sells.

1) The strategy entered a position it should have never entered in the first place -or-

QUOTE:

1) The strategy entered a position it should have never entered in the first place -or-

QUOTE:

This is exactly the leg I'd want to optimize, filtering these signals.

You guys are messing up this topic. I thought this topic was about getting out early on a bad position. Now you're saying it's not. I'm confused. (And then another poster wants to discuss a feature request.)

On entering positions, regardless of how good your entry leg is, your strategy is going to mistakenly enter a bad position. And you cannot fix that. You can look for good "value" if you're investing long term, but for trading it's kind of a crap shoot. The best you can do is avoid some bad positions.

My recommendation for avoiding bad positions would be to subscribe to one of these AI services that tracks sentiment for stocks. Am I allowed to mention names in this forum? But this also means writing both an on-demand data plugin and an event plugin for WL to bring this information into WL. The service I'm thinking of also costs $100/mo, so it's expensive. But if it makes money, then it's worth it.

Alternatively, you could try to use the Kalman filter on both price and volume data. But this is a dynamic system modeling problem and not everyone here is a control systems engineer. The other issue is that this problem is bigger than just price and volume data. There are many other outside factors governing market behavior, and that's why the AI service (mentioned in the previous paragraph) makes better sense.

This topic has diverged rather than converged. I suggest we close this topic and start two new ones:

1) A feature request to build a Performance Visualizer to assess the "buy leg" of the Execute block separately from the "sell leg". That should rattle a lot of users. And there are numerous ways to approach that.

2) A better way to analyze a "potential" entry position independent of using price and volume data (which only tells 25% of the story).

I've been reluctant to bring up either can of worms (above) because I have other projects at hand. But both issues have been at the back of my mind. Someone needs to go first and start these topics.

I am working on an extension which is able to find

a) The best available filter for entering a trade in the strategy at hand.

b) a measure whether it is better to exit a trade or keep it open.

It is already rather complete but needs some more time until it is releasable.

a) The best available filter for entering a trade in the strategy at hand.

b) a measure whether it is better to exit a trade or keep it open.

It is already rather complete but needs some more time until it is releasable.

Interesting news!

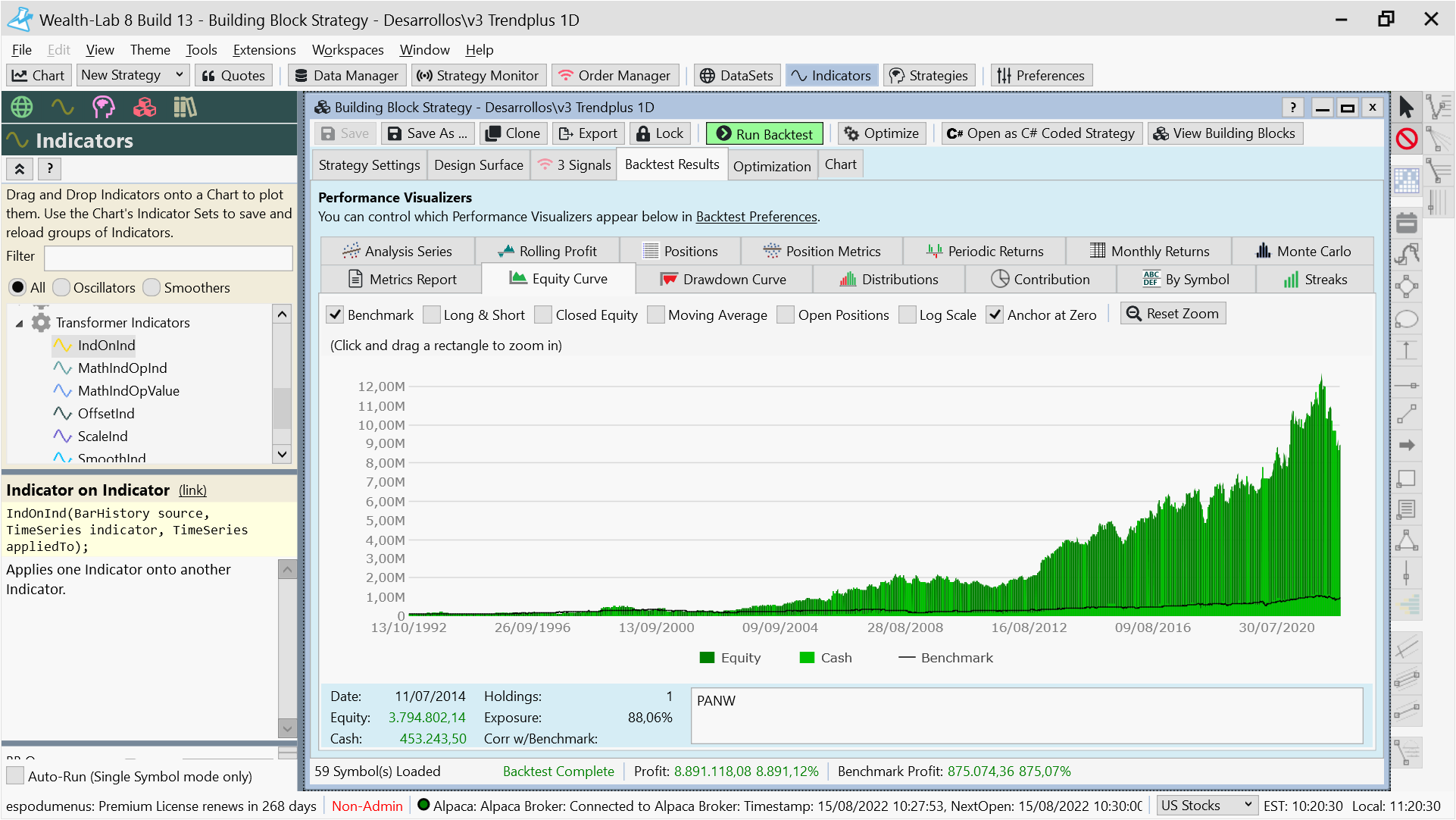

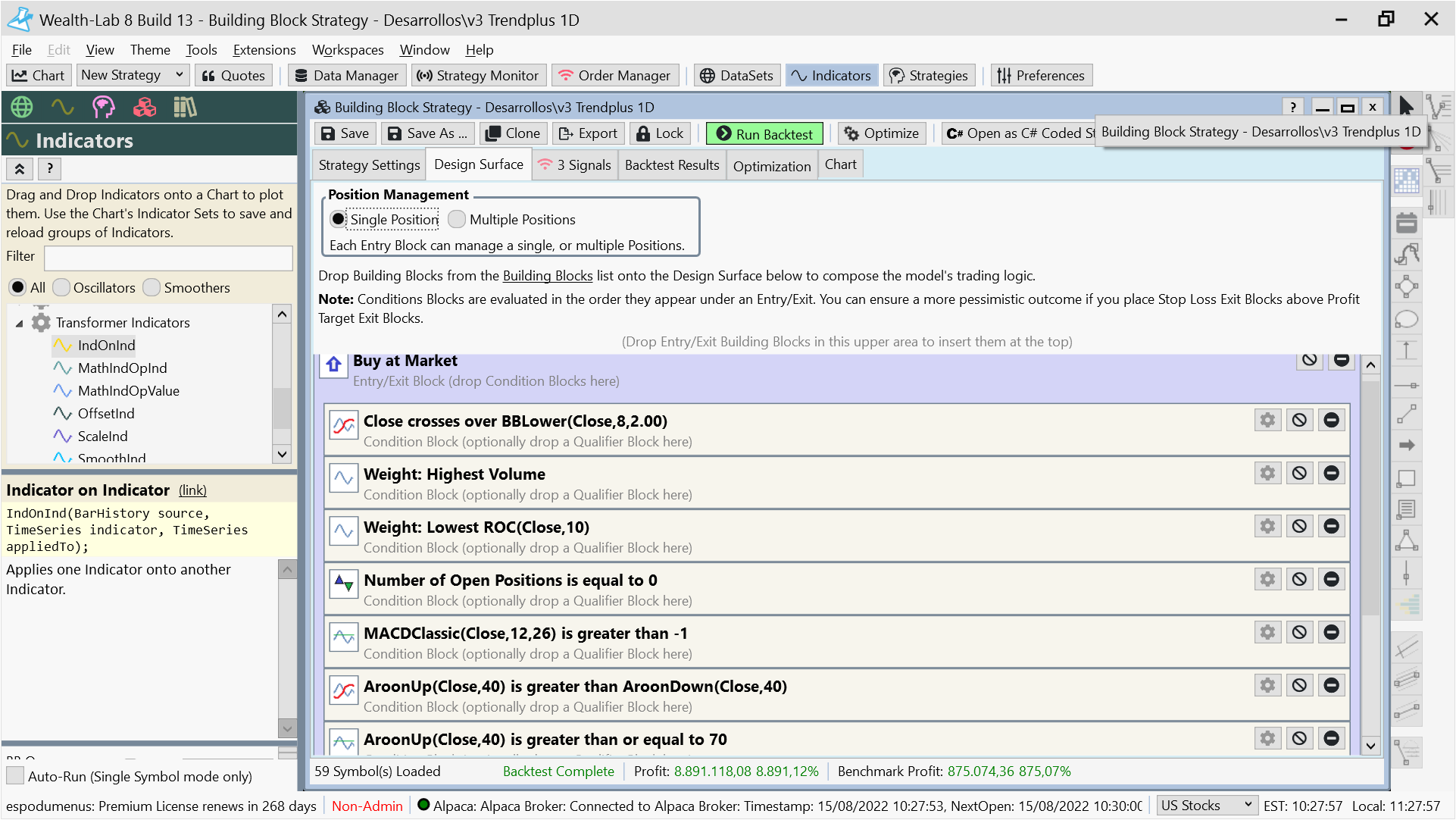

Next images are the BB Strategy with both exits based on BB and also a trailer SL. I want to reduce the enormous DD (during 30 years backtesting). I will try to divide the entry legs onto varions periods according to ATR (expressed in %) or according to Close versus 200 MA, and optimeze separately for each of these periods.

Your Response

Post

Edit Post

Login is required